Why Income Isn’t the Biggest Hurdle to Retiring Young

Would you believe me if I told you that most millionaires don’t earn six-figure incomes? It’s true, and it’s exactly why income isn’t the biggest hurdle to retiring young.

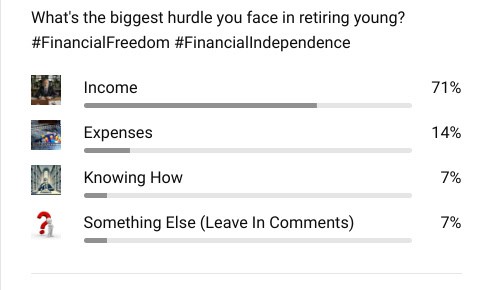

Recently, I ran a survey on our YouTube channel asking, “What’s the biggest hurdle you face in retiring young?” The results were striking: 71% of people believe that income is the primary obstacle.

Many think a higher income is the key to financial independence and early retirement. Or they blame their low income for their lack of assets. Statistics and my personal experience tells a different story.

I started with just $800 in savings and didn’t make over $50,000 a year until I was in my 30s. Yet, by my late 30s, I was a liquid millionaire. The key wasn’t my income, but how I managed my money.

In this post, I’ll disprove the income myth and show you what really keeps people from building wealth. I’ll also show you can overcome these obstacles.

Table of Contents

The Income Myth: Why Earning More Doesn’t Guarantee Wealth

Its been proven time and time again. A higher income is not needed for wealth. There are several reasons why this myth exists, and why it’s not reality.

The Illusion of High Income Equals Wealth

It’s easy to assume that earning more money will solve all your financial problems. But in reality, income is just a tool. What matters is how you use that tool.

Nearly 78% of American workers live paycheck to paycheck, according to a CareerBuilder study, and this includes many high-income earners. If income alone were the key to wealth, this wouldn’t be the case.

Lifestyle Inflation: The Silent Wealth Killer

As people earn more, they tend to increase their spending. This concept is known as lifestyle inflation. You might upgrade to a bigger house, buy a new car, or indulge in more frequent vacations.

While these upgrades can feel like deserved rewards, they can also keep you from building wealth. In fact, 40% of high-income earners (those making $100,000 or more annually) are still living paycheck to paycheck, according to Bankrate.

Earning more without managing your spending often means you’re no better off than someone earning far less.

Related: If You Always Want More, You Will Never Be Happy

High Income, Low Net Worth

Simply having a high income does not guarantee financial stability. In fact, nearly 1 in 5 households earning over $150,000 annually have a net worth under $250,000, according to research from The Federal Reserve’s Survey of Consumer Finances.

Without careful management of your earnings, it’s easy for expenses to rise and consume even a substantial salary, leaving you with little to show in terms of actual wealth.

Insights from The Millionaire Next Door

So, if income alone isn’t the key to building wealth, what is? This brings us to the habits and mindsets shared by millionaires who didn’t rely on high salaries to amass their fortunes.

In their book “The Millionaire Next Door,” Thomas J. Stanley and William D. Danko reveal that most millionaires in the United States are not high-income earners. They’re ordinary people who have accumulated wealth through disciplined saving, frugal living, and prudent investing.

These millionaires often live in modest homes and drive used cars—defying the stereotypical image of wealth. Instead of focusing on displaying their wealth, they prioritize building it.

Stanley and Danko’s research shows that income is not the main determinant of wealth; instead, the key is living below your means and consistently saving and investing over time.

Related: The Millionaire Next Door: I Read It As a Teen And Made It Happen

Why High Income Alone Doesn’t Lead to Financial Independence

So why isn’t high income a leading indicator of early retirement.

The Spending Trap

It’s easy to fall into the trap of spending more as you earn more. Without a clear financial plan, your income can quickly be depleted by short-term desires like new gadgets, dining out, or upgrading your lifestyle.

This kind of uncontrolled spending is a common pitfall for high-income earners. The more you spend, the less you can save or invest, which delays your journey to financial independence.

High Income, High Debt

High-income earners often have easier access to credit and loans, leading to significant debt accumulation. Expensive homes come with large mortgages, luxury cars bring monthly payments, and lavish lifestyles rack up credit card debt.

A CNBC report found that 60% of millennials earning over $100,000 feel like they are living paycheck to paycheck. This is often due to large debt burdens that consume their income. Interest payments on debt can erode even a high salary, reducing the amount of money available for saving and investing.

Neglecting Investment Opportunities

Even those who earn high salaries can fall into the trap of neglecting investments. Without proper financial education, some high-income earners may invest in speculative ventures or fail to diversify their portfolios.

According to Northwestern Mutual’s Planning & Progress Study, 21% of Americans have no retirement savings at all—a figure that includes some high earners. Understanding how to invest wisely is crucial to turning income into long-term wealth.

The Real Obstacles to Wealth Accumulation

Lack of Financial Education

One of the biggest barriers to building wealth is a lack of financial literacy. According to a National Financial Capability Study, only 34% of Americans can correctly answer basic financial questions.

Without knowledge of fundamental concepts like budgeting, saving, investing, and managing debt, it’s hard to make informed decisions that lead to financial independence.

Financial education empowers individuals to take control of their finances and build wealth, no matter how much they earn.

Related: Teach your kid personal finance

Poor Financial Habits

Financial success is driven by consistent, disciplined habits, not just income. Overspending, failing to budget, and neglecting to save or invest are behaviors that can prevent wealth accumulation, regardless of how much money you make.

Behavioral Economist Dan Ariely found that poor financial habits, such as impulsive spending and emotional purchasing, are key reasons people fail to build wealth over time.

Consumer Culture and Social Pressure

Society often encourages overspending through advertising and social pressure. The desire to “keep up with the Joneses” or maintain a certain image can lead people to buy things they don’t need, often at the expense of their financial future.

According to a 2019 survey by the American Psychological Association, 72% of Americans report feeling stress about money, driven in part by societal expectations to spend.

My Journey to Financial Independence

My own journey proves that wealth can be built without a high income. I started investing in real estate with just $800 and focused on managing my finances carefully.

I developed disciplined financial habits, avoiding bad debt, living below my means, and making smart investment decisions. These choices allowed me to grow my wealth, even when I wasn’t earning a high salary.

I became a liquid millionaire in my late 30s despite not making more than $50,000 a year at my job until I was 30. While my colleagues were upgrading their cars or buying expensive gadgets, I stuck to my modest budget, bought a reliable used car, and kept my living expenses low.

This choice gave me the breathing room to invest and build real wealth over time.

So how do you become financially independent if you have a low income? Here’s how I did.

Living Below My Means

One of the most important strategies I adopted was living below my means. I prioritized needs over wants and avoided unnecessary expenses. I lived in a modest home, drove used cars, and carefully considered each purchase, ensuring it provided long-term value.

This approach allowed me to save a significant portion of my income, even when my earnings were modest.

Consistent Saving and Investing

Despite earning under $50,000 annually for much of my career, I made saving and investing a priority. I set up automatic transfers to savings and investment accounts, ensuring consistency.

Over time, these small contributions grew through the power of compound interest. My disciplined approach to investing—maximizing my retirement accounts and diversifying my portfolio—was essential to growing my wealth.

Side Hustle

The phrase side Hustle didn’t exist when I started my journey. I invested in real estate when I was 21. I knew that people with low income could become financially free by having their money make money.

That was a lesson I learned from The Millionaire Next Door. Statistics support that self made millionaires tend to have multiple income streams, and not just their salary. So I bought rental houses. Over the next 20 years, tenants paid them off.

Continuous Financial Education

Recognizing the importance of financial literacy, I invested time in learning about personal finance. I read books, attended seminars, and followed experts who provided valuable insights.

I became a Chartered Financial Analyst (the hardest financial designation to get). I also had several Finra licenses like the Series 7, 63, 65, and 66.

The more I learned, the more control I had over my money. This ongoing education empowered me to make informed financial decisions that aligned with my goals.

Strategies for Building Wealth Regardless of Income

Create and Stick to a Budget

One of the most powerful tools for managing your money is a budget. By tracking your income and expenses, you can see where your money is going and identify areas where you can cut back.

A solid budget ensures that your spending aligns with your long-term financial goals.

Prioritize Saving and Investing

Treat saving and investing as non-negotiable. Pay yourself first by setting aside a portion of your income for savings before you spend on anything else.

Automate your contributions to savings and investment accounts, and start as early as possible to take full advantage of compound interest.

Live Below Your Means

Resisting lifestyle inflation is key to accumulating wealth. Keep your standard of living consistent, even as your income grows.

By directing additional income into savings and investments rather than spending it on luxuries, you’ll build wealth faster.

Avoid Unnecessary Debt

Avoid taking on new debt whenever possible and work to eliminate any existing debt. Debt, especially high-interest debt, can be a significant drain on your income. By paying off debt, you free up more money for wealth-building activities like investing.

Create Multiple Income Streams

Find ways to create multiple income streams. There are many ways to do this. My preferred way was investing in real estate. But your way might be different. The point is by having more income streams, you make more money. You also learn a lot more about the value of money.

Invest in Financial Education

Financial literacy is a critical factor in achieving financial independence. By continuously educating yourself, you empower yourself to make informed decisions and maximize your financial potential.

Avoid Fake Gurus: Fake Guru. Why Should I Listen to DadisFire?

Related: “Do Something That Makes You Go To The Library”

High-Income Earners Actually Tend To Struggle Financially

Let’s beat a dead horse here. People with high salaries tend to struggle with their money.

It’s easy to assume that earning a high salary guarantees financial stability, but even those with prestigious, high-paying jobs such as doctors, lawyers, and executives often face significant financial challenges.

A high income may create the illusion of wealth, but the reality is that poor financial management, significant debt, and high expenses can leave these professionals living paycheck to paycheck, despite their impressive earnings.

Doctors: A Late Start and Heavy Debt

Doctors, especially specialists, often earn six-figure salaries, but their financial lives are far from simple. According to the Association of American Medical Colleges (AAMC), the average medical school graduate leaves school with over $200,000 in student loan debt.

While physicians can earn substantial incomes, sometimes well into the $250,000 to $400,000 range, this financial burden can take years, or even decades, to repay. In addition to student loan debt, doctors face other financial pressures.

Their earnings are often delayed because they typically don’t start earning significant incomes until their early 30s, after completing medical school, residency, and fellowships. This delayed start means they miss out on nearly a decade of potential earnings compared to peers in other fields.

Doctors often face high living expenses due to societal pressures. There is a common expectation that they live in upscale neighborhoods, drive luxury cars, and maintain a certain lifestyle, which can push them toward overspending.

The long hours and high-stress nature of their work can also lead to spending on luxuries or experiences to reward themselves for their hard work.

On top of this, doctors, especially those in private practice, deal with significant business costs. These include expenses such as malpractice insurance, office rent, and administrative costs, which further eat into their income.

A Medscape survey revealed that 45% of physicians live paycheck to paycheck, and 49% believe they are behind on saving for retirement. Despite high earnings, late starts, significant debt, and high expenses mean many doctors struggle to build wealth.

Lawyers: Student Debt and Lifestyle Pressure

Lawyers also face financial challenges despite earning high incomes. According to The National Center for Education Statistics, the average law school graduate accumulates about $145,000 in student loans.

While lawyers at top-tier firms may start with salaries around $190,000, many others, especially those in smaller firms or public service, earn significantly less.

In addition to student debt, lawyers incur business-related costs such as maintaining a bar license, continuing legal education, and paying for malpractice insurance, all of which add to their financial burden.

Like doctors, lawyers often start their careers later than professionals in other fields due to the time required to complete law school and pass the bar exam. This delayed start in earning means they have less time to accumulate wealth before retirement.

Like doctors societal pressures also affect lawyers, who may feel compelled to project an image of success by purchasing expensive homes, cars, and other luxury items.

The combination of delayed earning, student debt, and high personal and professional expenses leaves many lawyers financially insecure. A Lawyer Salary Survey by ABA Journal found that 56% of lawyers feel financially insecure despite their high incomes, illustrating that high earnings alone are not enough to ensure financial stability.

Professional Athletes: Fast Money, Fast Decline

Athletes, especially those in the NFL, NBA, and MLB, often earn millions during their short careers. For example, the average salary in the NFL is around $2.7 million per year, while the average NBA player earns about $7.7 million annually.

Their financial challenges are unique. The short career spans of athletes—just 3.3 years in the NFL and 4.5 years in the NBA mean they must stretch their earnings over an entire lifetime. Without proper financial planning, many athletes find themselves facing financial instability soon after retirement.

One of the primary reasons for this is poor financial advice. Many athletes are unprepared for the complexities of managing large sums of money and often fall victim to risky investments or scams.

Without proper guidance, athletes can quickly deplete their earnings. The pressure to maintain a lavish lifestyle can be overwhelming. Athletes frequently spend on luxury homes, cars, vacations, and often feel obligated to support large groups of friends and family, further draining their resources.

A Sports Illustrated report found that 78% of NFL players are either bankrupt or in financial distress within two years of retirement, while 60% of NBA players face financial ruin within five years of leaving the league.

Despite large salaries, many athletes struggle financially due to short career spans, poor financial decisions, and excessive spending.

Executives and Entrepreneurs: High Earnings, High Expenses

Corporate executives and successful entrepreneurs often earn substantial incomes, sometimes well into the six or seven figures. High earnings don’t always translate into financial security.

Entrepreneurs, for example, may need to reinvest heavily into their businesses, which can result in financial risk. Even high-earning business owners may face cash flow issues, debt, or even business failure.

In the corporate world, many executives receive part of their compensation through stock options, which ties much of their wealth to the performance of the stock market, making them vulnerable to its fluctuations.

I worked with many of these executives at two of the largest financial services firms in the US. They are all still working despite making 10x more than me a year. Sometimes more. Yet they were leading the companies that give financial advice to millions of Americans.

Maybe they should have listened to my advice instead of their own?

In addition to business-related expenses, lifestyle inflation affects executives and entrepreneurs just as much as other high earners. There is often pressure to live in luxurious homes, drive high-end cars, and send children to private schools, all of which add to personal expenses.

These guys would talk about their Porsche collections before meetings, or their airplanes. Then they would complain about not being able to retire. They all still had to work. I had a Japanese car with 200,000 miles and a house that cost only twice my salary.

The demands of their careers may also lead to increased personal spending on travel, dining, and networking events. Despite earning large incomes, these individuals can find themselves financially vulnerable due to high spending and the volatility of their business ventures.

A 2018 study by Bloomberg revealed that 1 in 5 corporate executives lives paycheck to paycheck, and 30% lack sufficient savings to cover three months of living expenses. Their high earnings are often consumed by lifestyle costs and business-related expenses.

The bottom line is that high income alone is not enough to ensure financial security. Even those who earn substantial salaries can find themselves in financial distress without proper financial planning and disciplined spending habits.

The key to long-term financial success isn’t how much you make—it’s how you manage it.

What’s The Biggest Hurdle In Retiring Young

So, let’s go back to my survey. I would argue, and I am living proof, that knowing how is the biggest hurdle to retiring young. Our schools do not teach financial education, and there is so much bad advice on the internet. There is also this self sabotaging behavior and desire to keep up with the Jones’.

Low income doesn’t keep people from retiring young. Knowing how to make money out of money is the answer to financial freedom. Well that and having that money make more than your expenses for the rest of your life.

Conclusion: Redefining the Path to Wealth

The belief that a higher income is the key to financial independence is a myth. While income is a factor, it’s not the most important one.

Financial behaviors—such as living below your means, saving and investing consistently, avoiding unnecessary debt, and educating yourself—are the true drivers of wealth.

My own journey from starting with $800 to becoming a liquid millionaire shows that financial independence is achievable, even without a high income. By managing your money wisely and making deliberate financial decisions, you can overcome the real obstacles to wealth and achieve early retirement.

Take Action Today

I challenge you to start today. Take 10 minutes to review your spending habits—are you living below your means? Set one small financial goal this week, whether it’s automating your savings or cutting out an unnecessary expense. Every step you take now is a step closer to your financial independence.

Remember, it’s not how much you make, but how you manage your money that determines your financial success. Take control of your financial future today and begin your journey toward financial independence.

🙋♂️Ready to take charge of your financial future? Subscribe to the DadisFIRE newsletter and follow Dad is FIRE on YouTube for more insights on financial independence and smart money management.💪