10 Credit Card Myths Debunked by a Finance Expert (With 830+ Credit Score)

Credit cards can either build your financial strength or quietly drain it, it depends on how you use them. Most people don’t realize that the problem isn’t the card itself, it’s the misinformation around it.

Bad advice and old-school money fears have created some of the biggest credit card myths still floating around today.

I’m going to debunk those credit card myths in this article. But why listen to me?

Table of Contents

Why Listen To Me?

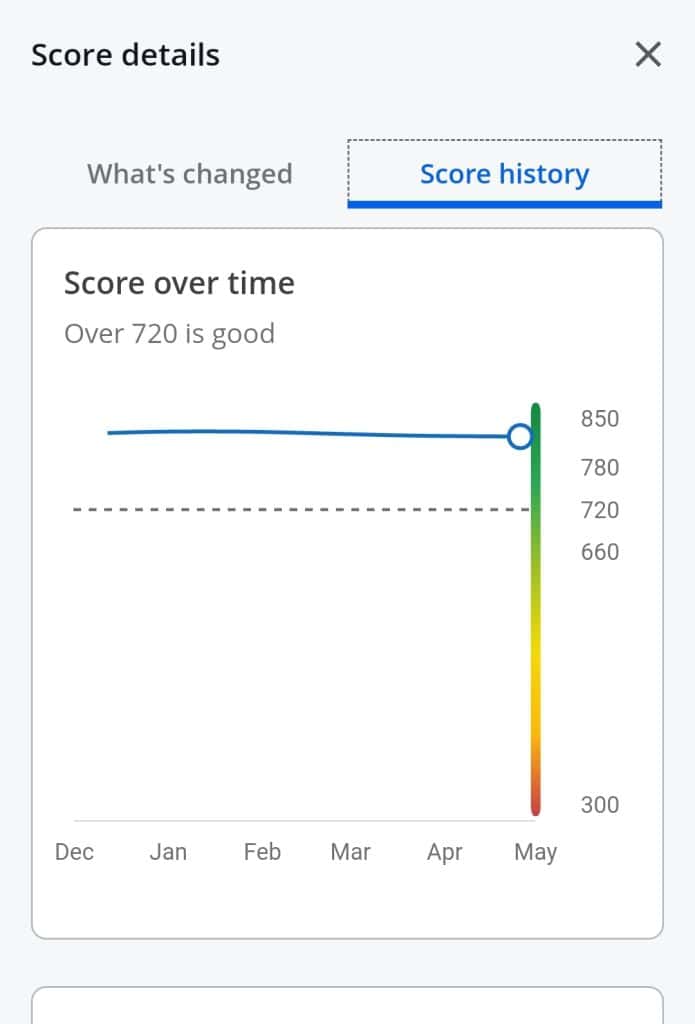

I am a Chartered Financial Analyst with more than 20 years of experience in Financial Services.

I have had a credit score in the 800s from when I made $25,000 without a penny to my name to today. I also retired at 42 a few years ago.

My wife’s credit score was in the 500s when we met 10 years ago. It’s in the 830s now.

So this is something I know a thing or two about. The image is my score.

Credit Cards Always Lead to Long Term Debt

There’s a common belief that credit cards are a straight path to debt. Stories of people falling into massive debt due to reckless spending are everywhere.

According to Experian, the average credit card balance in the U.S. is $5,525. But this is one of the most persistent credit card myths, and it doesn’t have to be your reality.

When used responsibly, credit cards can be a valuable tool. They offer convenience, security, and rewards. The key is to understand how to use them without building debt.

Personally, I love credit cards because it makes budgeting easier for me. I know here every penny goes. But that takes discipline.

Set a budget and stick to it. Pay off the balance in full each month. Use credit cards for planned purchases.

Related: My 5 year old girls opening their first bank account

Carrying a Balance Improves Your Credit Score

Many believe that carrying a balance can boost their credit score. This is a misconception. Carrying a balance means paying interest, which is unnecessary.

According to FICO, payment history accounts for 35% of your credit score, and amounts owed (including credit utilization) account for 30%.

Credit scores are calculated based on various factors. Payment history and credit utilization are the most significant. Carrying a balance does not positively impact these factors.

Keep credit utilization below 30%. Pay bills on time. Monitor credit reports regularly.

Related: 13 Things You Can’t Do (Easily) With a Bad Credit Score

Closing Old Credit Cards is Good for Your Credit Score

Closing old credit cards can negatively affect your credit score. The length of your credit history is a significant factor. A longer credit history generally indicates responsible credit behavior.

When you close an old credit card, you reduce your overall credit limit. This shortens your credit history and can lower your credit score.

Reduce usage instead of closing. Keep cards active with small purchases.

The card I use every day is from the 1990s, when I was still in college.

Applying for Multiple Credit Cards Hurts Your Credit Score

It’s important to differentiate between hard inquiries and soft inquiries.

Hard inquiries occur when a lender checks your credit report as part of a credit application. Soft inquiries occur when you check your own credit or when a lender pre-approves you for an offer.

Applying for multiple credit cards in a short period can lead to several hard inquiries. This can temporarily lower your credit score, but this impact is typically temporary and small if managed wisely.

Space out credit card applications. Research and choose the best fit.

Related: How Many Cards Is Too Many? An Expert Answers.

Credit Cards Have Hidden Fees that Make Them Unworthy

Credit cards can come with various fees. These include annual fees, late payment fees, and foreign transaction fees. But these fees can often be avoided or minimized with careful management.

They are also never hidden. You just have to read the terms.

Choose no-annual-fee cards, set up autopay to prevent late charges, and pay attention to billing cycles. The more you understand your card, the less you’ll ever pay.

Related: 25 Hidden Fees Draining Your Money (And How to Avoid Them)

Credit Cards Are Only for Big Purchases

Some people think credit cards should only be used for major expenses. That’s another outdated credit card myth that limits how much value you can get from using them.

Using your card for regular spending, groceries, gas, utilities, helps you earn rewards and build credit at the same time. It can also simplify budgeting since everything’s tracked in one place.

Use credit cards for everyday purchases. Track spending through monthly statements. Redeem rewards for routine expenses.

Related Video: Credit Card Secrets According To Expert With 800+ Credit Score 💳🔥

Credit Card Rewards Are Not Worth the Effort

Another common belief is that credit card rewards aren’t worth the trouble. That’s one of the most misleading credit card myths out there. While some programs can be complex, many are simple and offer real value for families.

Many families have found that credit card rewards can help offset costs for things like travel, groceries, and even cash back.

According to a study by the Federal Reserve, over 83% of credit card users with rewards cards redeem their rewards annually, which can lead to significant savings

Understanding the specific rewards structure of your credit card can maximize these benefits without much extra effort.

Research rewards programs before choosing a card. Use apps or tools to track rewards. Redeem rewards for maximum benefit.

Related: 14 Credit Score Myths Debunked by a Finance Expert

Using Credit Cards Will Harm My Financial Health

Some people believe that using credit cards will inevitably lead to poor financial health. This myth is often based on misunderstandings about how credit cards work.

Responsible use of credit cards can actually improve your financial health by helping you build credit, earn rewards, and manage cash flow. The key is to use credit cards within your means and pay off balances in full each month.

Set clear spending limits. Use credit cards for planned expenses. Monitor your account regularly.

Related: 13 Pieces of Bad Financial Advice That People Still Believe

Credit Cards Are Only for People with High Incomes

There’s a misconception that credit cards are only suitable for people with high incomes. In reality, credit cards can be beneficial for individuals and families at all income levels.

Credit cards can help manage cash flow, build credit, and provide a safety net for emergencies. Many credit cards offer rewards and benefits that can help lower-income families save money.

Look for credit cards with no annual fees. Use rewards to supplement income. Build credit to access better financial products.

Practical Tips for Families to Maximize Credit Card Benefits

Many credit cards offer rewards programs and cashback opportunities. These rewards can be used to offset everyday expenses or fund special family activities.

By using credit cards for routine purchases, families can accumulate rewards points or cashback. This can then be used to save money on future purchases.

Use points for family vacations. Look for travel benefits. Combine rewards with other savings strategies.

Related Video: 27 Credit Card Perks Most People Don’t Use (But Should)

Real-Life Examples of Smart Credit Card Use

A recent survey found that 47% of families using credit cards responsibly reported saving money through rewards and cashback. That alone proves how misleading some credit card myths really are.

Take a family that uses a rewards card for groceries. By paying the balance in full every month, they avoid interest and build points that cover a portion of their annual vacation.

Another family might use a cashback card for utilities and holiday shopping, earning money back on purchases they’d make anyway.

These examples show that when you ignore credit card myths and focus on smart strategy, you can turn ordinary spending into long-term financial advantages.

The way we do it is my wife has a card, I have a card, our business has a card, and we have a card for our utilities and recurring expenses. Each card has its own purpose.

Related: Is It Better To Separate Or Join Accounts With A Spouse?

The Truth Behind Credit Card Myths

Believing in common credit card myths can quietly cost you money and opportunities. Once you understand how credit really works, you can use it to your advantage instead of fearing it.

The truth is simple: credit cards aren’t the enemy. When you pay on time, keep balances low, and use rewards strategically, they become one of the best tools for financial growth and protection.

Seeing through these credit card myths helps you make smarter money moves, strengthen your score, and keep more of what you earn.

🙋♂️If you like what you just read, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube.💪

{kind=link}