Why Paying Off Debt Early Isn’t Always the Best Financial Move

“Get out of debt” is one of the most overused lines in personal finance, and it’s not wrong. But it’s also not the full story. Some debt will drain your money. Some can actually help build wealth.

Here’s the part no one tells you: over 70% of total U.S. household debt is in mortgages, and yet homeowners saw trillions in equity gains between 2019 and 2024. Debt didn’t ruin them, it helped build their net worth.

So it’s not just about having debt. It’s about what kind of debt you have, and what you’re doing instead.

Here’s how keeping low-interest debt can sometimes make more financial sense than paying it off early, especially when that money could be used to invest, build wealth, or improve cash flow.

Stick around, this is the side of debt “experts” usually skip. Also share it with who needs to see it.

Table of Contents

The Real Types of Debt: Smart vs. Toxic

Some debt builds wealth. Some destroys it. The difference? Interest rates, asset quality, and if it’s feeding your future or eating it.

This section breaks it down. If you’re holding the right kind of debt, paying it off early might not just be unnecessary, it might be a mistake.

“Good Debt” Isn’t a Myth

Good debt is typically low-interest, long-term, and attached to an appreciating or income-producing asset. Think mortgages, federal student loans with income-based repayment, and business loans tied to profitable operations.

For example, a 30-year fixed mortgage at 3.5% interest on a home that appreciates 5–6% annually can lead to significant gains, even after accounting for costs.

Student loans for high-ROI degrees (e.g., in engineering, IT, healthcare) are another form of productive debt. In each case, the debt acts more like an investment tool than a liability.

These types of debt also come with manageable repayment terms and potential tax advantages.

Mortgage interest is still deductible for many households, and student loan interest can reduce taxable income up to $2,500 per year (subject to income limits).

Video: My Mortgage Is Only 2.3%, Should I Pay It Off?

What Cheap Debt Really Costs You (Spoiler: Not Much)

When inflation is high, fixed low-interest debt becomes even cheaper in real terms. A mortgage at 3% during a 4–5% inflation cycle actually loses value each year, it gets easier to repay.

According to Statista, the household debt service ratio (monthly debt payments as a % of disposable income) was 9.8% as of Q3 2023. That’s well below its 2007 peak of over 13%.

Even though Americans are taking on more total debt, it’s becoming cheaper to carry in the context of income and inflation.

This is why blanket advice to “just pay it off” doesn’t always hold up. If the debt is low-cost and manageable, holding onto it while deploying your cash elsewhere can yield a better financial outcome.

Opportunity Cost: The Real Price of Paying Off Cheap Debt

Paying off debt early might sound like progress, but in some cases, it’s a poor trade-off. Every dollar used to reduce a low-interest balance is a dollar that’s not invested or saved elsewhere.

This is where opportunity cost comes in. It’s the money you miss out on when you prioritize debt reduction over wealth-building activities.

You Could Be Earning Instead

The stock market doesn’t guarantee returns, but it does reward consistency.

Over the past 50 years, the S&P 500 has returned an average of more than 10% annually. Even with down years, long-term investors typically outperform the interest saved by prepaying a 3–5% loan.

Let’s say you have a $300,000 mortgage at 3.25%. Paying it off early saves interest, but investing that same money over 15 years could easily net $100K–$200K more, depending on returns. That’s not a gamble. That’s math.

The key is understanding the spread. If your investment outpaces your loan’s cost, then prepayment isn’t just unnecessary, it’s inefficient.

Related: CFA Institute: 20 Common Investing Mistakes That Could Crush Your Portfolio

Liquidity Is Power

Cash equals options. And options are everything when life gets unpredictable.

Tying up funds in loan payoffs sounds noble until you hit a job loss, emergency, or market opportunity and have nothing liquid to work with. That’s a real risk.

Nearly 60% of Americans still can’t cover a $1,000 emergency from savings, according to a recent survey. That number hasn’t moved much in years.

Being debt-free on paper doesn’t help when your roof leaks and you can’t write a check. Keeping accessible cash, and keeping your debt costs manageable, is often the safer and smarter strategy.

Related: What Is The Right Amount Of Physical Cash You Should Keep at Home For An Emergency

How Strategic Debt Builds Wealth

Used correctly, debt doesn’t limit wealth, it multiplies it. The goal isn’t to avoid debt at all costs. The goal is to use it to control more valuable assets while keeping your own money working somewhere else.

Smart debt lets you scale what would otherwise take decades of saving. It buys time, access, and opportunity. And in some cases, the only real mistake is paying it off too soon.

Leverage in Real Estate

Real estate is one of the clearest examples of wealth built with debt. Most people can’t buy a home with cash, but a 20% down payment lets them control 100% of the property. That’s leverage, and it works both ways, but historically, it’s been in the owner’s favor.

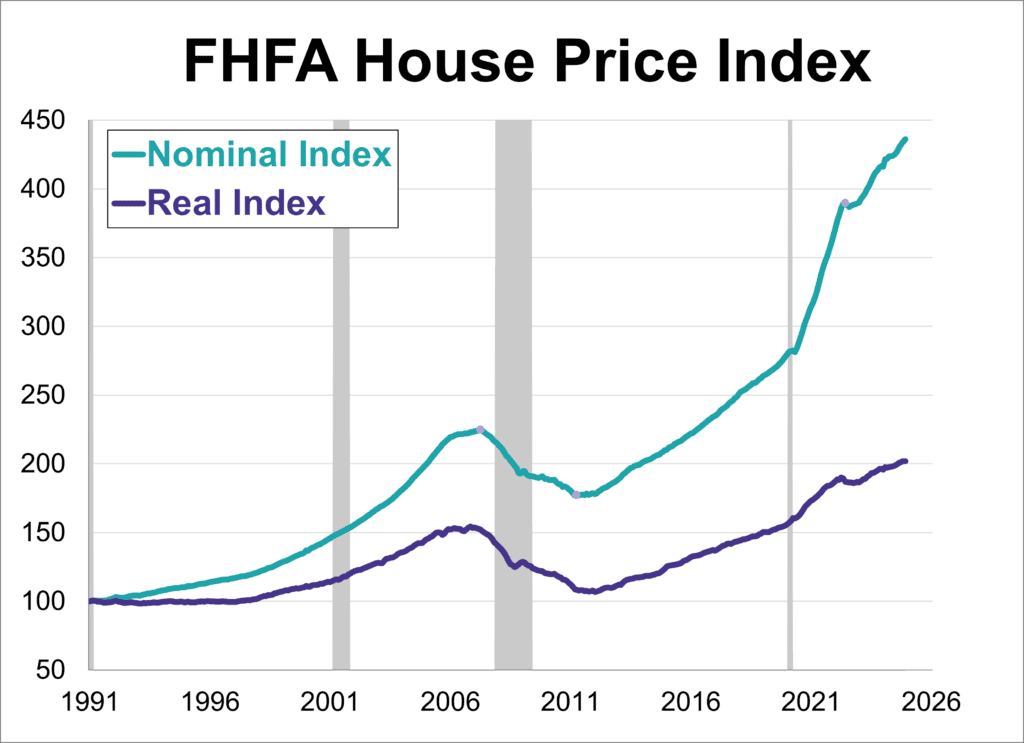

U.S. home values rose an average of 4.3% annually from 1991 to early 2025, according to data from the Federal Housing Finance Agency (FHFA).

Related: How to Get The Lowest Mortgage Rate (Even If People Think Rates Are High)

Using Debt to Fund Business or Investments

It’s not just real estate. Business owners and investors use debt to scale and they do it because it works.

According to the Federal Reserve’s 2024 Small Business Credit Survey, 59% of employer businesses used some form of financing to grow or stabilize operations. The most common reason wasn’t to cover payroll or emergencies, it was to expand.

A $50K business loan at 6% that helps generate $200K in new revenue isn’t a burden. It’s a smart trade.

The same logic can apply to investing: buying more stock with margin, using personal loans to fund real estate, or freeing up capital through asset-backed lines of credit. Riskier? Yes. But in controlled amounts, that risk is often worth the return.

The mistake isn’t using debt. The mistake is using it to buy things that don’t pay you back.

🙋♂️If you like what you are reading so far, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube.💪

When Paying Off Debt Makes Sense

There are still times when being aggressive with debt payoff is the right move. Not all debt is worth keeping, and in some cases, holding onto it does more harm than good.

The key is knowing which debt costs more than it’s worth, and when peace of mind is more valuable than a few extra points of return.

Toxic Debt Is a Financial Fire

High-interest debt doesn’t need a spreadsheet, it needs to go. Credit cards, payday loans, buy-now-pay-later schemes, and store-branded accounts often carry APR rates of 20–30%. That’s not leverage. That’s a money leak.

As of Q1 2025, the average credit card APR is 21.37%, according to LendingTree. That kind of interest grows fast and compounds in the wrong direction.

Unlike mortgage or business debt, these balances don’t come with asset growth, rental income, or tax advantages. They just grow.

In these cases, there’s no nuance. Pay them off. Then avoid them going forward.

Related: 23 Mistakes To Paying Off Debt That Keeps People Poor (And How to Fix Them)

Mental Simplicity Still Matters

Even with financially sound debt, some people just want it gone, and that’s valid. There’s a real psychological benefit to simplicity, especially for people who value minimalism, predictability, or are nearing retirement.

Being debt-free reduces risk, lowers monthly obligations, and provides peace of mind. But just be aware: that comfort has a cost. If you’re walking away from a 7% return to save 3%, understand the tradeoff.

There’s no wrong choice, just a more expensive one.

A Smarter, Balanced Strategy

The best debt strategy isn’t all or nothing. You don’t need to choose between being completely debt-free or leveraging everything to the hilt. Most people should land somewhere in the middle, paying down bad debt while still using good debt to move forward.

That balance lets you grow your net worth, keep liquidity, and reduce risk at the same time.

It’s not about being anti-debt or pro-debt. It’s about being pro-net worth.

Keep What’s Working, Kill What’s Not

Start by separating your debts into two camps: productive and destructive.

Productive debt is low-interest, fixed-rate, and tied to income or appreciating assets like a mortgage, a rental property loan, or a business line of credit. That’s debt you might keep.

Destructive debt includes anything with a high variable rate, no clear return, or no upside like credit cards, payday loans, or retail financing. That’s the stuff that needs to go. Fast.

Then get strategic. Keep minimum payments on the productive side and invest the difference elsewhere. Focus any extra income or windfalls on wiping out high-cost debt first.

It’s not just about peace of mind, it’s about putting your money where it compounds, not where it evaporates.

Video: Why A 15 Year Mortgage Makes More Financial Sense Than 30 Year Mortgages

Split the Difference: Pay Down and Invest

There’s no rule that says you can’t pay down debt and invest at the same time. In fact, that’s often the smartest move. It spreads your risk, grows your assets, and keeps your financial options open.

For example: if you’re deciding what to do with a $10,000 bonus, consider putting $5,000 toward extra mortgage payments or a car loan, and the other $5,000 into an index fund or high-yield savings.

One gives you guaranteed interest savings, the other keeps compounding. Both improve your position.

Debt is just a tool. And like any tool, it’s only as smart as how you use it.

Debt Isn’t the Enemy, Wasted Potential Is

Paying off debt feels responsible, but it’s not always the smartest financial move. Smart debt builds assets, protects liquidity, and keeps your money growing.

The real danger isn’t having a mortgage or business loan, it’s letting opportunity slip while chasing a zero balance. Use debt with intention, not fear.

The goal isn’t to owe nothing, it’s to own your time, your choices, and your future.

🙋♂️If you like what you just read, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube. 💪 Also be sure to follow DadisFIRE on Medium💰