Retiring With a Mortgage: When It Works and When It Doesn’t

There’s a rule a lot of people grew up hearing: pay off your mortgage before you retire. It sounds clean, simple, responsible. But these days, more retirees are walking into their golden years with a mortgage, and not all of them are losing sleep over it.

That said, the costs aren’t small. According to the Employee Benefit Research Institute, one in five average retirees spend 60% of their income on housing. That kind of ratio doesn’t leave much breathing room.

So what’s the real issue here? Is it the debt, the monthly bill, or the bigger financial picture?

In this article, we’ll break down real numbers, risk factors, and what it looks like to retire with a mortgage today. You’ll see what kind of retiree can actually handle it, and who needs to rethink the math.

👉 Keep reading, this might change how you think about mortgage debt in retirement.

Table of Contents

What Retirees Actually Spend (and Where the Money Goes)

Most retirement advice talks about how much to save. But spending is what actually determines how long the money lasts.

And the biggest expense in retirement? Still housing.

Average Monthly Spending in Retirement

The average retired household spends $4,345 per month. Around 81% of that goes to just five categories: housing, food, healthcare, transportation, and entertainment.

Other sources peg the total closer to $5,000 per month, based on lifestyle and location.

Investopedia lists housing, healthcare, and food as the top three categories, no surprise, especially with rising property taxes and medical premiums.

Related: Retirement Shock: 22 Expenses Some Boomers Might Struggle to Afford Soon

Housing: Still the #1 Expense in Retirement

A recent report shows that nearly 40% of retirees still carry a mortgage. And it’s not a small balance, the average mortgage is over $100,000, which translates to about $10,000 a year in payments.

Many of these loans will stretch out another 12 years or more, meaning housing continues to hit the budget hard long after the last paycheck.

Even retirees who paid off their homes still face taxes, insurance, and maintenance, costs that don’t go away just because the bank is out of the picture. But for those with active mortgages, it’s a fixed cost that takes priority over everything else.

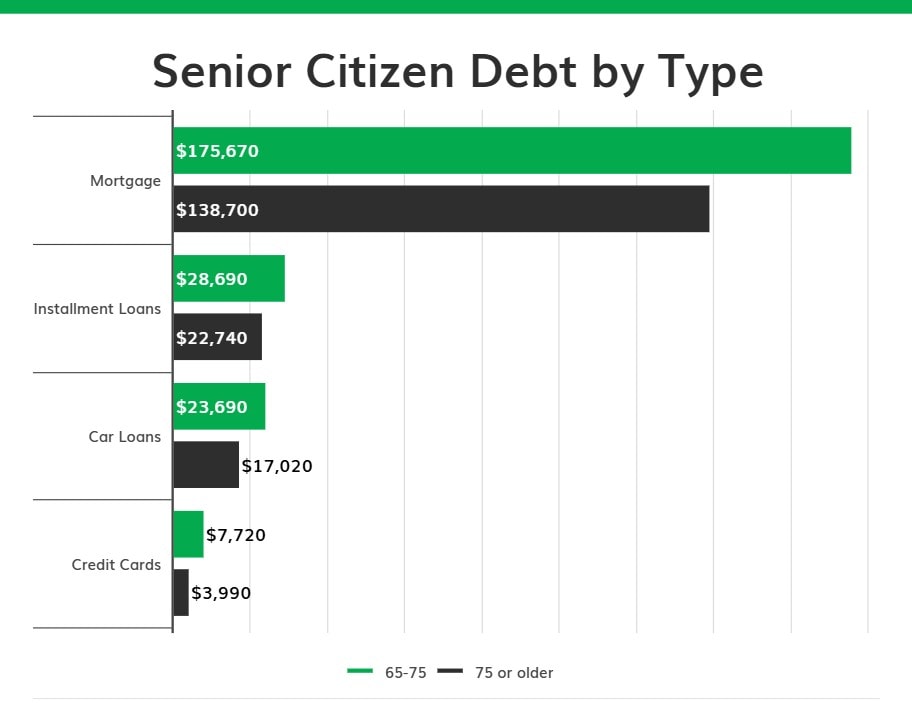

Total Debt Is Still a Big Part of the Picture

The mortgage gets all the attention, but it’s just one piece of the debt stack. Retirees today are still juggling credit cards, car loans, and other leftover balances.

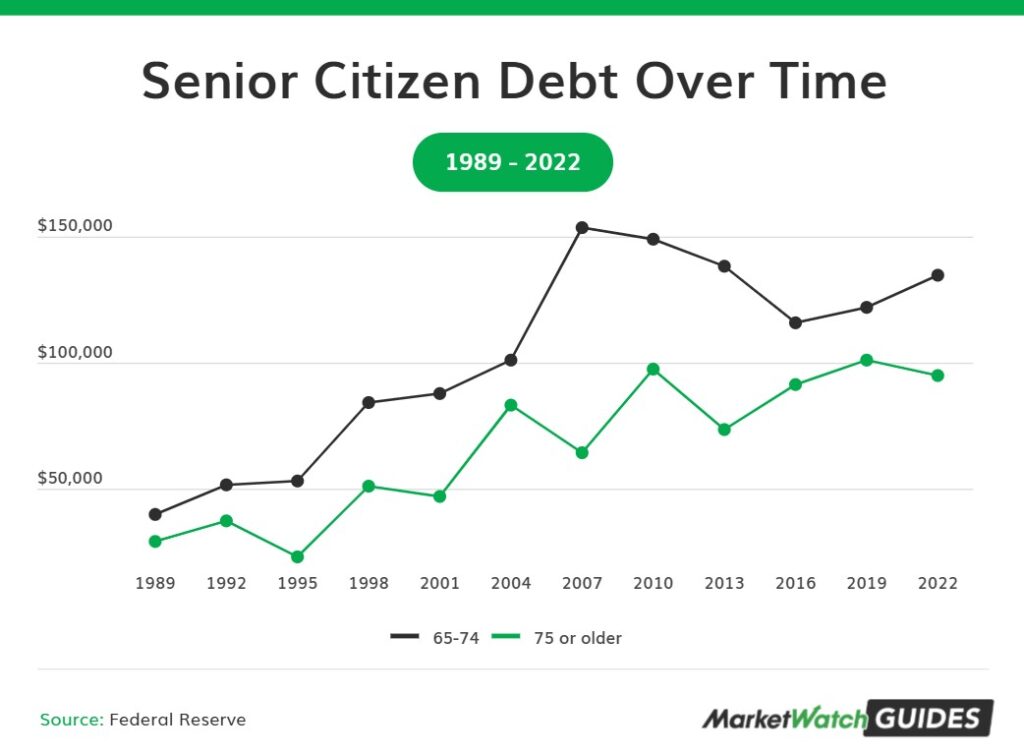

Based on recent figures, the average total debt for consumers aged 65 to 74 was $134,950 in 2022, compared to $94,620 for those 75 and older. That includes everything, not just housing.

It’s a sharp reminder that debt doesn’t always disappear when work ends.

Retirees who are still making multiple loan payments every month have less freedom to handle rising healthcare costs, inflation, or even just enjoy retirement without looking over their shoulder.

Should You Retire With a Mortgage?

It’s a fair question. Plenty of retirees do, and some manage just fine. But there are real trade-offs.

When a Mortgage Could Be a Problem

It’s not just about having debt, it’s about the pressure it puts on monthly income. On a fixed income, a mortgage payment can throw off the entire budget. You might need to pull more from retirement accounts just to cover the bills.

That means higher taxes, faster drawdowns, and less room for error.

Debt stress is real too. According to a 2023 AARP study, 65% of people 65 and older with debt consider it a problem, and 29% call it a major problem.

Even a low-rate mortgage can be stressful when you’re trying to stretch savings over 25 years.

Older homeowners today also carry more debt than previous generations.

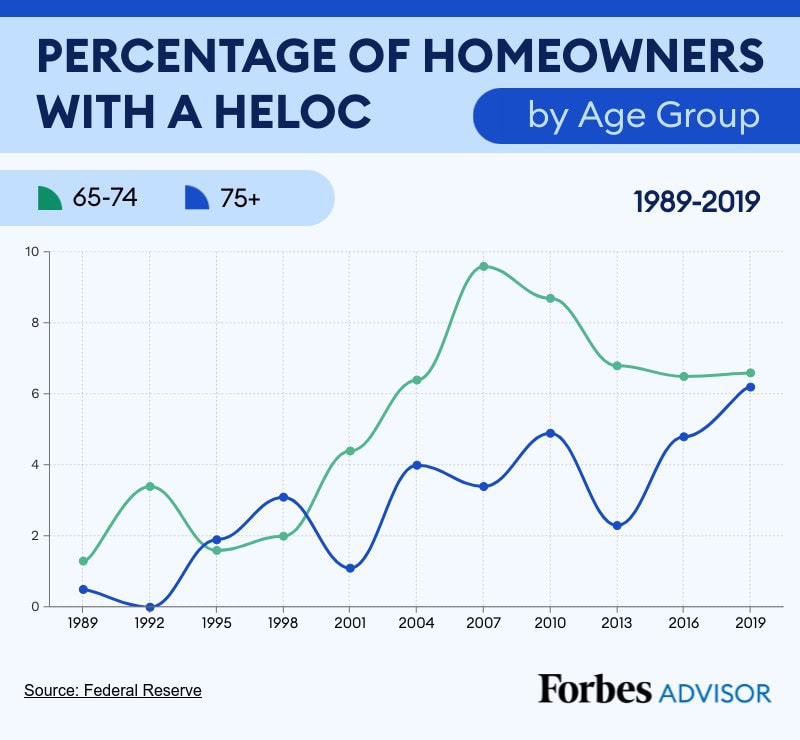

Federal Reserve data reported by Forbes confirms that more seniors now have a mortgage or HELOC than 30 years ago, and the average amount owed has grown.

Seniors are also more likely to tap home equity, increasing their exposure to interest rate swings.

When Keeping the Mortgage Makes Sense

Now, not all debt is toxic. Some retirees keep their mortgage because it actually helps their finances. If your rate is under 4% and your investments are earning 6–8%, paying off the house early could cost more than it saves.

There’s also the liquidity angle. For retirees with large tax-deferred accounts, pulling out a lump sum to kill the mortgage can trigger big tax bills.

Keeping the loan can help spread out withdrawals and reduce the annual tax hit.

Then there’s the emotional side, downsizing can be disruptive. For many, staying in a familiar home and neighborhood matters more than a clean debt sheet.

Video: My Mortgage Is Only 2.3%, Should I Pay It Off?

What Type of Retiree You Are Matters

Not all retirees carry the same financial weight. Income levels, debt tolerance, and spending habits shape how much risk a mortgage really brings.

Let’s break it down.

High-Income Retirees with Assets

For retirees with strong portfolios, holding a mortgage isn’t usually a crisis. They’ve got the reserves to float payments without selling off assets at the wrong time.

Some even use mortgages as a tax strategy, keeping their investments growing while paying low interest. They’re more likely to have long-term care coverage, backup cash, and access to financial advisors.

In this group, a mortgage is just another line item, not a threat.

🙋♂️If you like what you are reading so far, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube.💪

Middle-Income Retirees with Debt

This is where things get tighter. Middle-income retirees usually depend on Social Security and modest retirement savings. Add a mortgage to the mix, and things can get uncomfortable fast.

When housing eats up more than 30% of income, it’s a red flag, especially for someone on a fixed monthly check. The payments might fit on paper, but there’s little room left for rising insurance premiums, healthcare costs, or surprise repairs.

These retirees aren’t necessarily in crisis, but the margin for error is thin. One unexpected expense, a new roof, a hospital stay, a family emergency, can throw the whole plan off balance.

Keeping the mortgage works if everything else goes right. The problem is, retirement rarely runs on a smooth schedule.

Retirees Who Rent Instead

Renting might seem like a way to sidestep mortgage stress, but it’s not always cheaper.

U.S. Census data shows that over 21 million renter households spent more than 30% of their income on housing in 2023. That’s nearly half of all renters nationwide.

Without the benefit of equity growth or fixed payments, retirees who rent are more vulnerable to rent hikes and moving costs.

For many, keeping a mortgage, and the control that comes with it, can still be the better deal.

Related: Why Buying a House is Financially Better Than Renting (Includes Calculator)

Housing Debt Trends Among Seniors

Carrying debt into retirement used to be rare. Now it’s the norm. More seniors are holding onto mortgages and tapping equity lines than any generation before them, and the numbers show it’s not slowing down.

Mortgage Debt in Retirement Is No Longer Uncommon

Back in the ‘90s, the idea of a retiree with a mortgage was unusual. Today, it’s routine. Seniors are not only more likely to still have a mortgage, they’re also taking on larger balances than ever before.

In 2022, consumers aged 65 to 74 had an average home loan balance of $175,670, according to Federal Reserve data analyzed by MarketWatch.

For those 75 and older, the number was lower, $138,700, but still significant. That’s a lot of debt for someone living on retirement income.

Nearly a quarter of adults over 75 still had a mortgage in 2022, the highest percentage since 1989. And seniors are also more likely now to have a HELOC, using their home equity for repairs, living costs, or emergencies.

This shift reflects a different retirement mindset. For some, it’s strategic. For others, it’s out of necessity. Either way, housing debt has become a permanent part of the retirement equation.

Options to Consider Before You Retire with a Mortgage

If you’re not retired yet, this is where you get to play offense. The mortgage isn’t the problem, it’s what you do with it.

These are real moves that can put you in a stronger position before the paychecks stop.

Pay It Off Early, But Don’t Go Broke Doing It

If you’ve got the cash, wiping out the mortgage before retirement can bring real peace of mind. No payment means lower monthly expenses and less pressure on your investment withdrawals.

But this only works if you’re not draining your emergency fund or triggering big tax hits. Tapping your 401(k) or IRA to pay off a low-interest mortgage could cost more in taxes than you’d save in interest. And once that cash is locked into your house, you can’t spend it.

It’s worth considering, but only if it doesn’t drain your safety net.

Related: How To Pay Off Your Mortgage: I Have Paid Off A Mortgage Early Several Times

Refinance or Restructure While You Still Qualify

Once you retire, getting approved for a loan gets harder. If you’re still working and carrying a mortgage with a high rate or short term, now’s the time to adjust it.

You could refinance to lower the monthly payment or extend the term to give yourself breathing room. Yes, you’ll pay more interest over time, but that trade-off might be worth it if it means a more flexible retirement budget.

If your home’s value has gone up, some lenders will even let you restructure your loan to free up cash flow without selling.

Downsize Intentionally, Not Out of Panic

Selling a too-big or too-expensive house and moving into something smaller can make a huge difference. Smaller home, smaller taxes, smaller utility bills. The right move could cut your housing costs in half and let you bank the difference.

But downsizing isn’t just about price, it’s also about location, comfort, and lifestyle. If you end up trading a paid-off home for a new condo with high HOA fees, you may not be saving anything. Run the full numbers, not just the sale price.

And don’t wait until your budget forces the move. Make the decision while you’re in control.

Keep the Mortgage, But Set It Up Right

Sometimes keeping the loan is the smarter choice, especially if the interest rate is low and the investment accounts are earning more. But that strategy only works if your plan supports it.

You’ll need a budget that holds up even when the markets don’t, a cash buffer for repairs and surprise bills, and a withdrawal strategy that doesn’t leave you overexposed.

Ideally, set aside 6–12 months of mortgage payments in cash. That way, if your stocks are down or a tenant skips rent (if you’ve got rental income), you’re not scrambling.

Keeping a mortgage in retirement isn’t failure. It just means you need to manage it like any other risk. Plan around it, protect your cash flow, and make sure it doesn’t control your decisions later.

Mortgage or No Mortgage, Retirement Still Has to Work

A mortgage in retirement isn’t automatically good or bad, it’s just another line in the budget. What matters is how the rest of your plan holds up around it.

If the numbers make sense, the debt can stay. Just don’t let old rules decide what your future should look like.

🙋♂️If you like what you just read, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube. 💪 Also be sure to follow DadisFIRE on Medium💰