14 Credit Score Myths Debunked by a Finance Expert

Let’s talk about credit scores. Most people either ignore them or assume they’re some kind of scam. The truth? Your credit score is just a tool, and if you understand how it works, you can actually make it work for you.

An Experian survey found that only 72% of consumers even had a rough idea of their credit score. That means millions of people are making big money decisions without knowing one of the most important factors that affect their financial life.

Here are the biggest credit score myths people keep falling for, along with the credit facts that actually matter. Once you see how the system really works, you’ll know how to use it to your advantage instead of letting it hold you back.

Let’s clear this up once and for all. Share this with who needs to see it.

Table of Contents

Why Listen To Dad Is FIRE?

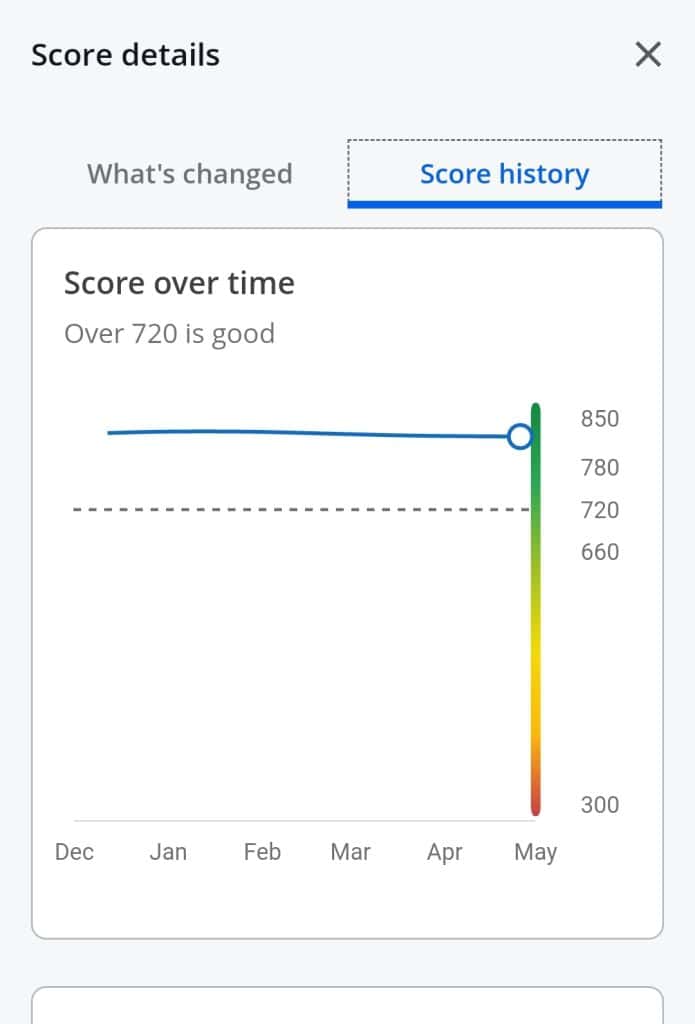

I’m a Chartered Financial Analyst with over two decades in financial services. My credit score has been in the 800s for more than half my life.

It was in the 800s when I was making $25k a year. It was in the 800s when I became a liquid millionaire at 38. It was in the 800s when I retired at 42. It is still in the 800s.

In the 12 years I have known my wife, her credit score has increased 300 points.

I understand credit scores.

If you want real credit advice from an expert, not recycled myths, you’re in the right place. The image above is my actual score.

Myth #1: Credit Scores Are Rigged

Credit scores aren’t rigged. They’re based on math, not magic. If your credit score is low, it’s because of your financial habits, not because the system is out to get you.

Late payments, maxed-out credit cards, and too many hard inquiries will wreck your score.

But the good news? Just like bad habits lower your score, good credit habits will raise it. Lenders aren’t grading you on personality, they’re looking at on-time payments and how you manage credit responsibly.

Play smart with your credit score, and you win.

Myth #2: Closing Old Credit Cards Helps Your Score

Think closing an old credit card will help your credit score? Think again. Your credit history length matters a lot. The longer you’ve had an account open, the better it looks.

That 10-year-old credit card you don’t use? Keep it open, even if it just sits in a drawer. It’s helping your score.

This makes sense too. It shows lenders you are stable because you have a long track record of being responsible.

Just make sure you use it occasionally so the issuer doesn’t close it for inactivity. Credit scores reward long, responsible history. Don’t cut yours short.

Myth #3: Any Hard Inquiries Destroy Your Score

Every time you apply for a loan, credit card, or even some utilities, the lender checks your credit score. That’s called a hard inquiry, and too many in a short period can drop your score.

One or two? No big deal. But five or six in a few months? Lenders start thinking you’re desperate for credit.

Be strategic. Only apply for credit when you actually need it. Otherwise, let your credit history do the work.

Related: Finance Expert (With 830+ Credit Score) Dismisses 10 Credit Card Myths

Myth #4: Checking Your Credit Hurts Your Score

Checking your own credit report does nothing to your credit score. That’s a soft inquiry, and it doesn’t count against you. What does hurt? Ignoring your credit report and letting errors or fraud go unnoticed.

You can check your credit report for free every year at annualcreditreport.com. Fix mistakes before they cost you.

Staying informed is the easiest way to protect your credit score.

Myth #5: You Need Debt to Have a Good Score

No, you don’t. You need credit, not debt. There’s a huge difference. You can have a great credit score without carrying a balance or paying a cent in interest.

Just use your credit card, pay it off in full every month, and keep your credit utilization low. That’s it.

Carrying a balance and paying interest isn’t “good for your credit.” It’s just good for the bank’s bottom line. Don’t fall for the myth.

Related Video: Bad Credit, Big Problems 13 Ways Your Score Might Be Holding You Back

Myth #6: Credit Scores Are Impossible to Improve

A bad credit score isn’t forever. Pay bills on time, keep credit card balances low, and limit new credit applications. That’s the formula.

Credit scores reward consistency, so don’t expect instant results.

Small, smart moves over time lead to big changes. Play the game right, and your credit score will climb.

Myth #7: A Higher Income Means a Higher Credit Score

Earning six figures won’t magically boost your credit score. Your income isn’t even factored into the formula. What matters is how you manage money: paying bills on time, keeping balances low, and handling credit responsibly.

Someone making $40,000 with great credit habits can have a higher credit score than someone making $400,000 who maxes out credit cards and misses payments.

It’s not about what you make, it’s about how you manage it.

Related: 16 Habits Common Among Frugal Millionaires and High Earners

Myth #8: Carrying a Small Balance Improves Your Score

This one refuses to die. Carrying a credit card balance doesn’t help your credit score, it just helps banks collect interest off you.

The best move? Use your credit card regularly, but pay it off in full every month.

This shows lenders you can manage credit without debt stacking up. Paying interest on purpose is like setting money on fire.

Keep your money, not the myth.

Myth #9: You Only Have One Credit Score

Nope. You actually have multiple credit scores. The most common one is your FICO score, but there’s also VantageScore and variations used by different lenders.

Your credit score can change depending on the version being used and the type of credit you’re applying for.

Mortgage lenders, auto loan companies, and credit card issuers may all see slightly different numbers. The key? Focus on good credit habits across the board, and all your credit scores will be solid.

🙋♂️If you like what you are reading so far, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube.💪

Myth #10: Paying Off Debt Instantly Fixes Your Score

Clearing debt is great, but your credit score doesn’t skyrocket overnight. It takes time. Your credit history, payment record, and credit utilization all play a role.

If you had high balances, paying them down will help, but the full impact may take months.

Lenders like to see a track record of responsible behavior, not just one-time fixes. The best credit scores are built with patience and consistency.

Related: 23 Debt Payoff Mistakes That May Keep You Broke (And How to Fix Them)

Myth #11: All Debt Is Bad

Debt isn’t the enemy, bad debt is. There’s a huge difference between maxing out a credit card on luxury purchases and taking out a low-interest mortgage for a home.

Credit scores reward responsible borrowing, not debt avoidance.

A well-managed mortgage, auto loan, or student loan can actually strengthen your credit mix. The goal isn’t to avoid debt completely, but to use it wisely.

Myth #12: You Can Pay Someone to Erase Bad Credit

If someone promises to “fix” your credit score instantly, run. Legitimate credit repair takes time and effort.

No company can legally remove accurate negative information from your credit report.

The only way to improve your credit score is to build better habits, pay bills on time, lower your debt, and dispute errors. Anything else is a scam.

Myth #13: Credit Scores Don’t Matter if You Don’t Borrow

Even if you never take out a loan or open a credit card, your credit score can still impact you. Landlords check credit before approving leases. Insurance companies use it to set rates. Even some employers look at credit reports when hiring.

A strong credit score makes life easier, even if you don’t plan on borrowing. Ignoring it won’t make it go away, it just limits your options down the road.

Related: How to not be a bad landlord. How to be a better landlord.

Myth #14: Bankruptcy Destroys Your Credit Forever

Bankruptcy is a financial reset button, not a life sentence. Yes, it will hit your credit score hard, and it stays on your credit report for up to 10 years. But you can still rebuild.

Many people start improving their credit score within a few years through responsible habits, paying bills on time, using secured credit cards, and keeping debt low.

It’s not ideal, but it’s not the end of the road.

Take Control of Your Credit

Credit scores aren’t out to get you, they follow a formula. Master the basics, make smart choices, and your score will rise. No need for gimmicks, just consistent habits that pay off.

Keep balances low, pay on time, and let time do the rest. Small moves lead to big results.

Now go take control of your credit score and make it work for you.

🙋♂️If you like what you just read, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube. 💪