17 Expert-Approved Ways to Improve Your Credit Score

Let’s talk credit scores. Some people obsess over them, others ignore them, but here’s the truth: your score controls a lot more than you think. Better rates, better approvals, more options.

The average FICO credit score in the U.S. is 717, according to the latest FICO data. That’s decent, but plenty of people are stuck with lower scores that make borrowing more expensive.

The good news? Small changes can lead to big improvements.

Here are the practical steps that actually help you raise your score, including simple habits, tricks to improve your credit score, and smart moves that strengthen your credit profile without taking on new debt.

Ready to take control of your credit? Let’s get into it.

Table of Contents

Why Listen To Me?

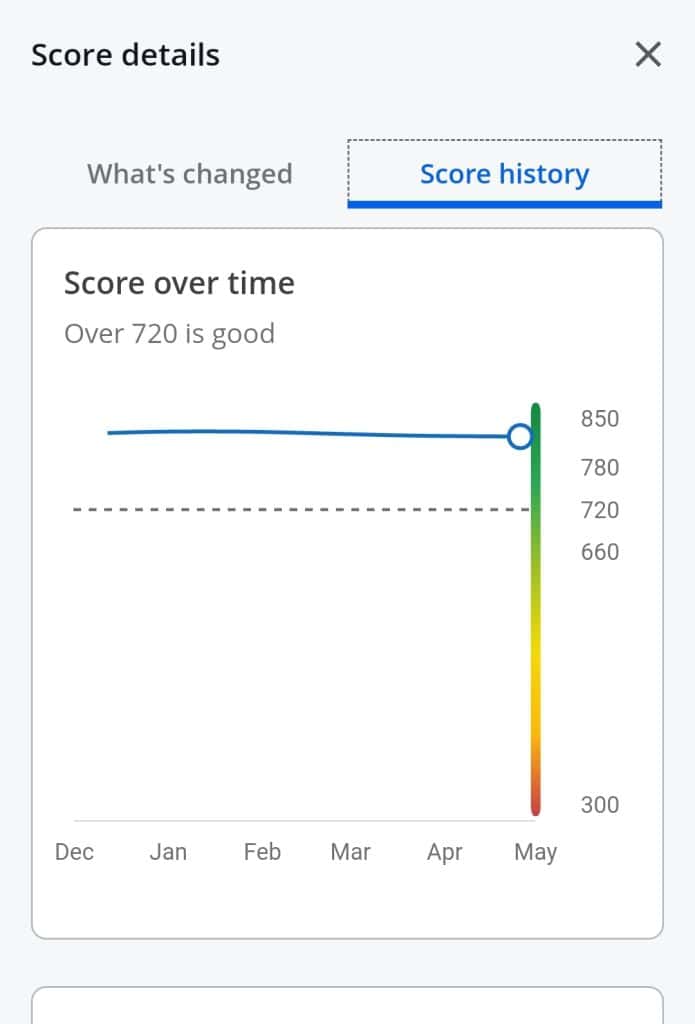

I’m a Chartered Financial Analyst with over two decades in financial services. My credit score has been in the 800s for more than half my life.

It was in the 800s when I was making $25k a year. It was in the 800s when I became a liquid millionaire at 38. It was in the 800s when I retired at 42. It is still in the 800s.

In the 12 years I have known my wife, her credit score has increased 300 points.

I understand how to improve credit scores.

If you want real advice that actually works, you’re in the right place. The image above is my score.

Related: 10 Credit Card Myths Debunked by a Finance Expert (With 830+ Credit Score)

Pay Your Bills on Time

Want a high credit score? Follow the formula. Pay your bills on time, every time. Nothing tanks a score faster than a late payment. Even one missed payment can stay on your report for years.

Set up autopay or reminders so you never forget. Being consistent with payments is the easiest way to keep your score strong.

Related: Expert (With 820+ Credit Score) Addresses 10 Credit Card Myths

Keep Your Credit Usage Low

Credit utilization is the amount of your balance relative to your credit lines. For example, if you have $1,000 in credit card debt and $10,000 in available credit, your utilization rate is 10%.

Keep that number as low as possible, under 30% is good, under 10% is even better. Pay off your balance in full each month to avoid interest and keep your score in top shape.

I pay mine off two or three times a month. I always have, even when I was a college student working in a factory.

🙋♂️If this is interesting so far, follow DadisFIRE on Medium, then hit like to see more articles on financial freedom, personal finance, and smart money moves.💪

Ask for Higher Limits (Without Spending More)

You can routinely ask for credit limit increases, which can improve your utilization rate overnight. More available credit means a lower percentage of usage, as long as you don’t increase your spending.

A higher limit doesn’t mean free money, it’s a tool to make your credit profile look better. Some issuers let you request an increase online, while others require a call. Just be smart and use it to your advantage.

Related: 22 Common Expenses You Can Actually Negotiate to Save More Money

Don’t Close Old Accounts

The longer your credit history, the better your score. Closing old accounts shortens that history and can lower your available credit, both of which can hurt you.

Even if you don’t use an old card much, keep it open with an occasional small purchase. This keeps the account active and helps your credit age naturally.

If an issuer closes a card due to inactivity, you lose that history. Let time work in your favor instead of cutting your credit short.

Related: I Retired Young: 25 Things I Know, That Most People Never Figure Out

Limit Hard Inquiries

Every time you apply for credit, lenders pull your report, which temporarily lowers your score. A single inquiry isn’t a big deal, but too many in a short period make you look desperate for credit.

Space out applications to avoid unnecessary dings on your score. If you’re shopping for a loan, do it within a short timeframe, multiple inquiries for the same loan type within a few weeks usually count as one.

Be strategic about when you apply, especially if you’re working on raising your credit score fast or improving credit approval for big purchases.

Related: Rich vs. Broke: 18 Financial Moves That Make the Difference

Check Your Credit Report

Mistakes on your credit report can cost you, and they happen more often than you’d think. A late payment that wasn’t yours or an account you never opened can drag your score down.

You’re entitled to a free credit report every year at annualcreditreport.com, use it. Look for errors, outdated information, or signs of identity theft. If something’s wrong, dispute it immediately to get it fixed.

Staying on top of your credit report is an easy way to protect your score.

Related Video: Credit Score Myths vs. Reality: What Actually Matters According To Credit Expert

Use Credit, Don’t Let It Use You

Credit scores reward responsible use, not debt. You don’t need to carry a balance or pay interest to build good credit. Use your credit card for small purchases, then pay it off in full each month.

This keeps your utilization low, avoids unnecessary interest, and proves you can manage credit wisely.

Having different types of credit like a credit card, car loan, or mortgage can help, but don’t take on debt just for a score boost. The goal is to use credit as a tool, not a trap.

Keep Your Credit Card Accounts Active

Credit card issuers can close inactive accounts, which can hurt your score. If a card sits unused for too long, you could lose the credit limit and the positive payment history tied to it.

Use each of your cards at least once every few months for a small purchase like gas, groceries, a streaming subscription, then pay it off in full. This keeps the account active and helps maintain a longer credit history.

Losing old accounts can shrink your available credit, which increases your utilization rate. Keeping them open and active helps your score stay strong.

🙋♂️If you like what you are reading so far, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube.💪

Become an Authorized User

If you have a trusted family member with a strong credit history, ask to be added as an authorized user on their card. Their account history gets added to your credit report, which can help improve your score.

You don’t even have to use the card, they can keep it, and you still benefit. Just make sure they’re responsible with payments, because missed payments on their end can hurt you too.

This is one of the easiest ways to build credit fast, especially if you’re just starting out. A good credit piggyback can go a long way.

Related: Save on Taxes: 19 Smart Ways to Keep More of Your Money

Rebuild the Smart Way With a Secured Card

If your credit score needs serious work, a secured credit card is a great way to rebuild. Unlike regular credit cards, secured cards require a refundable deposit, which becomes your credit limit.

Use it responsibly, make small purchases and pay the balance in full each month. Over time, this builds a solid payment history, and many issuers will upgrade you to an unsecured card once you’ve proven yourself.

Secured cards are a reliable option for anyone trying to raise credit score fast or climb out of a low score without risking new debt.

Related: Stealth Wealth: The Key to Keeping Your Wealth and Your Freedom

Set Alerts So You Don’t Slip

Staying on top of your balances is key to managing your credit. Many banks and credit card issuers let you set up alerts that notify you when your balance reaches a certain level.

This helps you keep your utilization low and avoid overspending. If you know you’re approaching the 30% threshold, you can make an early payment to keep your score in check.

Small habits like this add up over time and make managing credit easier. Staying aware of your spending keeps your score moving in the right direction.

Related: 25 Hidden Fees Draining Your Money (And How to Avoid Them)

Pay Off Collections the Right Way

If you have old debts in collections, paying them off the wrong way won’t help your score. Before paying, request a “pay-for-delete” agreement, some collection agencies will remove the negative mark if you pay the balance.

If that’s not an option, paying still looks better than an unpaid collection, but it won’t erase the damage overnight. The good news? The impact of collections fades over time, especially as you build better habits.

Handle past mistakes smartly, and focus on the future.

Related: 23 Debt Payoff Mistakes That May Keep You Broke (And How to Fix Them)

Don’t Open Too Many Accounts at Once

Every new credit account comes with a hard inquiry, which temporarily lowers your score. Opening multiple accounts in a short period makes you look risky to lenders. Stick to only applying for credit when you need it.

If you’re building credit, space out new accounts by several months to let your score recover. A few well-managed accounts are better than a bunch of new ones dragging your score down.

Be patient, and your credit will grow the right way.

Automate Everything You Can

Life gets busy, and missing a payment because you forgot is an easy mistake to make. Set up autopay for at least the minimum payment on all your accounts to avoid late fees and credit damage.

You can always make extra payments manually, but autopay gives you a safety net. Pair it with balance alerts and calendar reminders for full control over your credit.

Automating the basics helps you maintain good credit and supports any long-term plan to raise your credit score fast through consistent habits.

Related: Don’t Set It And Forget It: 20 Bills That Should Not Be on Autopay

Freeze Your Credit If You’re Not Using It

You don’t need to be paranoid, just smart. If you’re not planning to apply for new credit anytime soon, freezing your credit file can block fraud without hurting your score.

It’s free, takes just minutes, and stops anyone, including identity thieves, from opening accounts in your name. If you need to apply later, you can temporarily lift the freeze.

This move protects your credit profile and gives you peace of mind while you build.

Switch to Weekly Micro-Payments

Here’s a hack most people overlook: pay your credit card down weekly instead of monthly. Your balance gets reported based on the statement date, not your payment date.

So if you pay early and often, your utilization rate looks much better, even if you spend the same amount. It’s simple math, and it’s one of the easiest tricks to improve your credit score without changing your actual spending.

Related: 15 Expenses That Secretly Eat Your Money Every Month

Get Rent and Utility Payments Reported

You’re already paying rent, utilities, and your phone bill. Might as well get credit for it. Some services like Experian Boost or RentTrack let you add these payments to your credit report.

It won’t turn a 580 into an 800 overnight, but it can give you the edge if you’re just starting out or rebuilding. It’s one of the few legit ways to raise your score without taking on new debt.

Just be consistent and let your payment history do the work.

Related: 19 Frugal Home Hacks That Instantly Save You Money

Win the Credit Score Game

Credit scores aren’t as complicated as people make them seem. Follow the right habits, stay consistent, and your score will climb. Pay on time, keep balances low, and be smart about new credit.

Small moves add up, and patience wins the game. Lenders reward responsibility, not tricks.

Take control, play it smart, and let your credit work for you.

🙋♂️If you like what you just read, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube. 💪 Also be sure to follow DadisFIRE on Medium💰