13 Signs You’re Ready to Buy Your First Home

Buying your first house isn’t about perfect timing, it’s about readiness. The market’s noisy, advice is all over the place, and most people are still guessing.

In this gallery, we’ll walk through the signs you’re actually ready to buy a home, financially, mentally, and practically.

👉 Tap or Click through the slides to see if you’re ready for homeownership.

Table of Contents

Majority of Americans Think It’s a Bad Time to Buy a House

Nearly 80% of Americans say it’s a bad time to buy a home, according to a 2024 report. That’s a record level of pessimism, and a lot of it comes from fear, headlines, and rising rates.

But here’s the thing: most of those people aren’t actually looking to buy. If you’ve done the math and your situation checks out, you might be in a better position than most.

👉 Tap or Click ahead to see if you’re one of the few who’s truly ready to buy your first home.

You’re Ready to Handle Homeowner Headaches

When the toilet breaks or the AC stops blowing, there’s no landlord to call. That’s not a dealbreaker, it’s just part of owning. If you’ve got the patience (and the cash cushion) to handle repairs, you’re ready.

Owning a home means fixing what you’d usually ignore, if that doesn’t scare you, that’s a green flag.

15 EASY Home Maintenance Tasks to Do Monthly (Before Something Breaks)

You’ve Got a Plan for the Down Payment

If you’ve got 20% saved, great, but it’s not a dealbreaker if you don’t. First-time buyers can qualify for FHA, VA, and other low-down-payment options.

I used no money down strategies to buy houses, so I know it’s possible when the numbers work. The key is having something saved, and knowing what loan options fit your situation.

Down payment is just part of the story. Being prepared is what really matters.

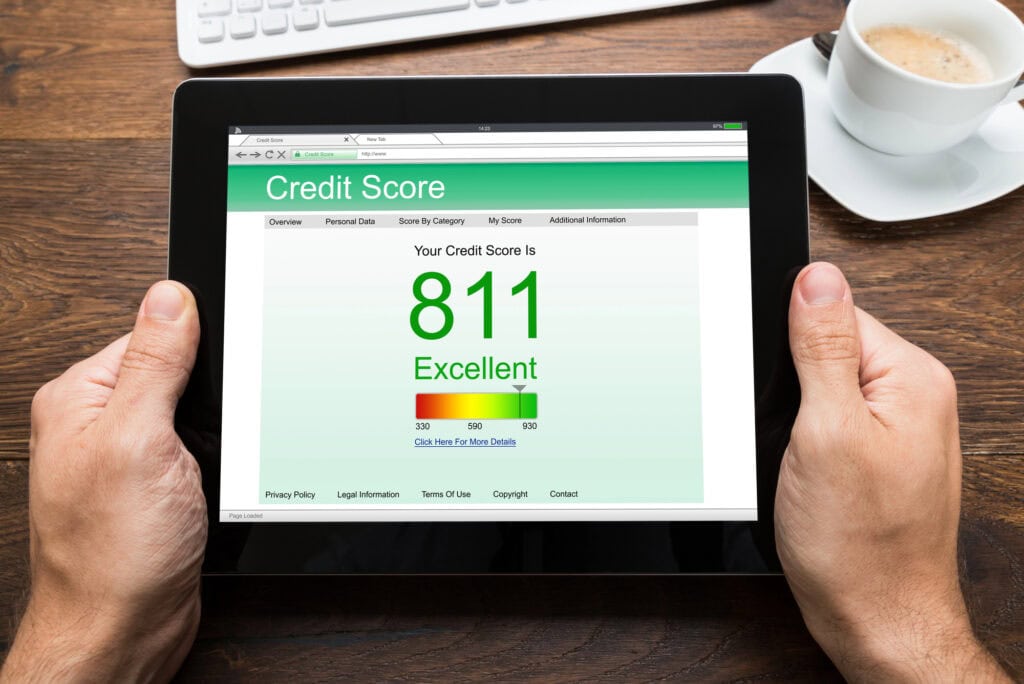

Your Credit Score Can Get You a Decent Rate

A credit score over 720 opens up the best mortgage deals. Even scores in the high 600s can work, but you’ll pay more over time. If you’ve been monitoring your score, lowering your utilization, and avoiding big new debt, you’ve already done the work.

Now lenders will take you seriously, and you’ll pay less for the same house.

Finance Expert (With 830+ Credit Score) Dismisses 10 Credit Card Myths

You’ve Built a Solid Emergency Fund

Before you take on a mortgage, you need a strong emergency fund, not just a little padding. The unexpected will happen in homeownership: busted pipes, broken furnaces, layoffs, or life curveballs.

Cash reserves don’t just help with emergencies, they help you make better decisions under pressure.

Your Job and Income Are Steady

Lenders want to see a two-year history of steady income in the same field or job. But this isn’t just about the bank, it’s about you feeling secure. If your paycheck is predictable and your field isn’t volatile, you’re ready to take on fixed housing costs.

A stable job means you’re not just buying a house, you’re building your foundation.

You’ve Researched Interest Rates and Monthly Costs

It’s not just about knowing the mortgage rate, it’s about knowing your monthly number. Taxes, insurance, HOA dues, and maintenance need to fit your lifestyle.

If you’ve plugged in the numbers and you’re still excited, that’s a good sign. You’re not guessing, you’re planning.

🙋♂️If you like what you are reading so far, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube.💪

You Know the Area, and Want to Stay

Buying only makes sense when you’re settled. If you’ve lived in your city for a couple years and see yourself staying at least five more, that’s a solid base. You know the neighborhoods, traffic patterns, and local costs.

That kind of familiarity reduces regret and helps you choose a home that fits you, not just the price.

You’re Tired of Paying More to Rent Than Own

The average rent in the U.S. hit $1,642 last month, according to Redfin. If that number’s higher than what a mortgage would cost in your area, it’s time to stop bleeding money. Rent offers flexibility, but no equity and no long-term gain.

When rent stings more than it frees you, it’s a signal, it’s time to buy something that pays you back.

Why Buying a House is Financially Better Than Renting (Includes Calculator)

Your Debt-to-Income Ratio Looks Healthy

Lenders look at your debt-to-income ratio (DTI) before anything else. If your total monthly debts (loans, cards, etc.) eat up less than 36–43% of your gross income, you’re in decent shape to get approved.

Even if your ratio is slightly higher, solid credit and stable income can still make it work. If your budget can handle a mortgage and you’ve proven it over time, that’s a green light.

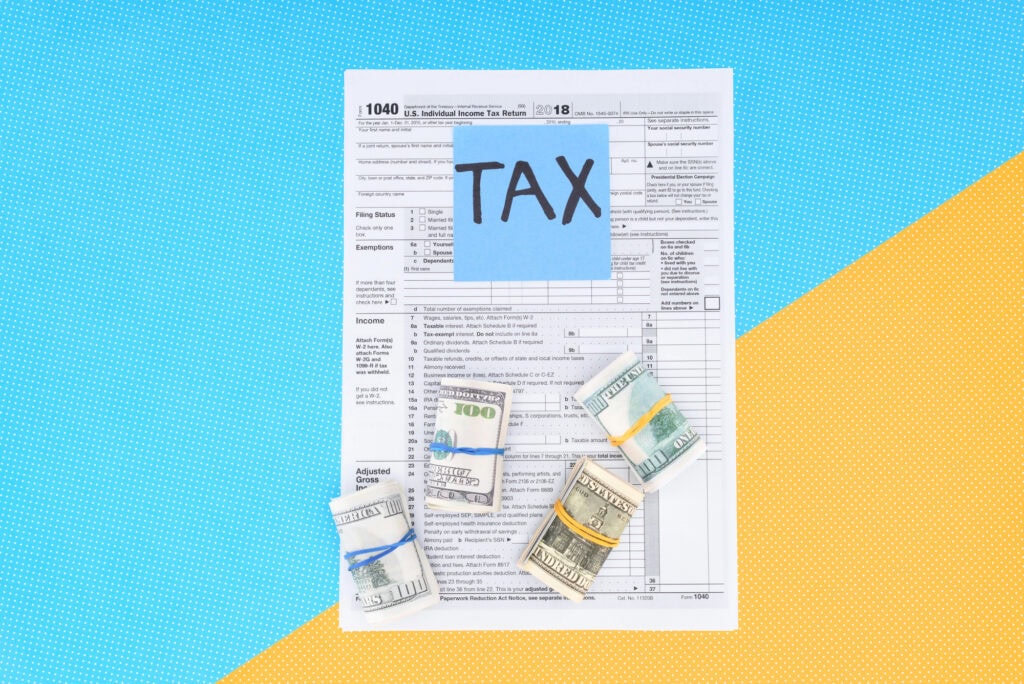

You Want the Tax Perks and Equity Growth

Owning a home can bring tax benefits, including mortgage interest and property tax deductions, if you itemize. More importantly, each payment chips away at the loan and builds equity.

That’s forced savings you don’t get when renting. If you’re thinking long-term wealth instead of just monthly costs, you’re on the right track.

24 Easy To Get Tax Breaks That Lower Your Taxes Without Itemizing

You’re Ignoring the ‘Bad Time to Buy’ Crowd

The National Association of Realtors says the average age of today’s homebuyer is 56, a record high. That’s how long some people are waiting. But real readiness isn’t about market timing, it’s about personal timing.

If the math works and your life lines up, ignoring the headlines might be your smartest financial move.

You’ve Run the Numbers, and Still Want the House

When you’ve built a budget that includes all homeownership costs, and you still want in, that’s a solid indicator. Too many first-timers get caught up in emotional decisions.

But if you’ve looked at utilities, repairs, furniture, and even moving costs and it still pencils out, you’re thinking like an owner, not a shopper.

We also made this related Video: When Is The Best Time To Buy A House (I’ll Tell You)

You’re Mentally Ready for the Responsibility

Buying isn’t just about spreadsheets, it’s about being ready for permanence. If you’re excited about mowing your own lawn or painting your own walls, you’re not just financially ready, you’re mentally there.

Homeownership adds responsibility, but also freedom. If that balance excites you, you’re ready to carry the keys.

Buying Your First Home Starts With Knowing You’re Ready

If you’re nodding along with more than half of these signs, you’re not far off. Buying your first home isn’t just about the market, it’s about being financially prepared, mentally ready, and long-term smart.

Most people wait until it feels safe, but the truth is, preparation beats perfect timing.

Run the numbers, trust the signs, and take the next step if it fits. The door’s more open than you think.

🙋♂️If you like what you just read, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube. 💪 Also be sure to follow DadisFIRE on Medium💰