Why a Roth IRA Isn’t Always the Best Choice: A Campfire Conversation

I was sitting around the campfire last weekend, enjoying the warmth of the flames and the comforting crackle of burning wood.

My cousin, a financial advisor brimming with enthusiasm, leaned over and brought up a topic that’s been buzzing incessantly on social media: Roth IRA conversions. He insisted that I should convert my Traditional IRA into a Roth IRA.

This conversation immediately struck a nerve. Everywhere I turn online, it seems like Roth IRAs are being hailed as the ultimate retirement solution for everyone, as if they’re a one-size-fits-all remedy.

My cousin, without any knowledge of my specific financial situation, was adamant about the benefits of a Roth conversion for me.

It reminded me of one of the most frustrating aspects of my career in financial services: the tendency of some financial advisors to make recommendations without proper discovery.

We started to argue. I maintained that a Roth IRA isn’t appropriate for me, while he insisted it was the best move. His certainty without understanding my income, assets, or financial goals was not just presumptuous but also a stark example of misguided advice.

It’s crucial for financial advisors to discover a client’s unique situation before dispensing recommendations, yet here he was, overlooking that fundamental step.

As the embers glowed and the night grew darker, our debate intensified. It became clear that this wasn’t just about us but about a broader misconception that Roth IRAs are inherently the best choice for everyone.

Let’s unpack this topic, explore what Roth and Traditional IRAs are, and discuss when each is appropriate, or not.

Table of Contents

Understanding Roth IRAs

A Roth IRA is an individual retirement account funded with after-tax dollars. This means you pay taxes on the money before it enters the account, but the growth and future withdrawals are tax-free, provided certain conditions are met.

The allure of a Roth IRA lies in its promise of tax-free income in retirement. If you expect to be in a higher tax bracket in the future, paying taxes now at a lower rate could be advantageous.

Roth IRAs don’t require you to take minimum distributions at a certain age, offering more flexibility in retirement planning.

There are income limits for contributing directly to a Roth IRA. For 2023, single filers with a modified adjusted gross income (MAGI) above $153,000 and joint filers above $228,000 are ineligible to contribute directly.

There are strategies like backdoor Roth conversions for high earners, but these come with their own complexities.

Understanding Traditional IRAs

A Traditional IRA, on the other hand, is funded with pre-tax dollars, assuming you meet certain conditions. Contributions may reduce your taxable income in the year you make them, offering an immediate tax benefit.

The funds then grow tax-deferred until you withdraw them in retirement, at which point they’re taxed as ordinary income.

Traditional IRAs come with Required Minimum Distributions (RMDs), which, as of 2023, must begin at age 73 due to the SECURE Act 2.0. This means you are obligated to start withdrawing a certain amount each year, whether you need the money or not, and pay taxes on those distributions.

When Is a Roth IRA Appropriate?

Roth IRAs can be a powerful tool in certain situations. They’re particularly beneficial if:

- You Expect Higher Taxes in Retirement: If you believe that your tax rate will be higher in retirement due to increased income or potential tax law changes, paying taxes now can save money in the long run.

- You Have a Long Time Horizon: Younger investors can benefit from decades of tax-free growth, amplifying the benefits of a Roth IRA.

- Estate Planning Is a Priority: Roth IRAs can be passed on to heirs without the burden of income taxes, and beneficiaries can stretch distributions over their lifetimes.

- You Seek Flexibility: Since contributions (not earnings) can be withdrawn at any time without taxes or penalties, Roth IRAs offer a level of flexibility that Traditional IRAs do not.

For instance, a 30-year-old professional expecting significant income growth might find a Roth IRA advantageous. They can lock in their current tax rate, enjoy tax-free growth, and avoid RMDs, providing both flexibility and potential tax savings.

When Is a Traditional IRA Appropriate?

Traditional IRAs may be more suitable if:

- You Expect Lower Taxes in Retirement: If you anticipate a drop in your income during retirement, deferring taxes until then could result in a lower overall tax burden.

- You Need Immediate Tax Relief: High earners may benefit from the immediate tax deduction that Traditional IRA contributions can provide, reducing current taxable income.

- You’re Subject to Income Limits: If your income is too high to contribute to a Roth IRA directly, a Traditional IRA might be your only option for tax-advantaged retirement savings.

- Cash Flow Is a Concern: Reducing your taxable income now can improve your current cash flow, which might be crucial for meeting other financial obligations.

Consider someone nearing retirement who currently earns a high income but expects their income—and consequently their tax rate—to decrease significantly upon retiring.

For them, a Traditional IRA offers immediate tax benefits and the prospect of paying less tax on withdrawals later.

When a Roth IRA Doesn’t Make Sense

Despite their benefits, Roth IRAs aren’t universally the best choice. Here are situations where a Roth IRA might not be appropriate:

Significant Assets in Taxable Accounts

In my case, my wife and I have a lot in taxable accounts from the sale of all of our paid off rental houses. We also have plenty in retirement accounts thanks to maxing out 401ks when we worked.

Having substantial assets in both taxable and tax-deferred accounts provides a natural hedge against tax rate fluctuations. It allows us to strategically manage withdrawals in retirement to minimize tax liabilities.

By diversifying the tax treatment of our assets, we can adapt to whatever tax landscape the future holds.

Lower Tax Bracket in Retirement

Many people find themselves in a lower tax bracket during retirement due to reduced earned income. According to data from the Tax Policy Center, the majority of households over 65 fall into lower tax brackets because they no longer receive substantial wages or salaries.

This means that deferring taxes until retirement, as with a Traditional IRA, can result in paying less tax overall.

In our situation, our current combined income covers our expenses comfortably. Upon full retirement, our income is likely to decrease, placing us in a lower tax bracket.

Paying taxes now at our current rate through a Roth conversion doesn’t make financial sense when we can defer and potentially pay less later.

High Current Income

Converting a Traditional IRA to a Roth IRA involves paying taxes on the converted amount in the year of the conversion. For individuals or couples with a high current income, this additional taxable income can push them into an even higher tax bracket, leading to a substantial and possibly unnecessary tax bill.

For us, adding a large Roth conversion to our income could significantly increase our tax liability for the year. This immediate cost outweighs the potential future benefits, especially when we consider our expected lower income in retirement.

Required Minimum Distributions (RMDs)

While Roth IRAs do not have RMDs during the original owner’s lifetime, Traditional IRAs do require distributions starting at age 73. Some view RMDs as a drawback, but they can be managed strategically.

If the RMDs aren’t needed for living expenses, they can be reinvested in taxable accounts or used for charitable contributions through Qualified Charitable Distributions (QCDs), which can satisfy the RMD requirement while reducing taxable income.

In our case, we plan to manage RMDs by aligning them with our financial needs and charitable goals, mitigating the tax impact while supporting causes we care about.

The Cost of A Roth Conversion

The tax bill associated with converting a Traditional IRA to a Roth IRA can be substantial, especially if you don’t have funds outside the IRA to pay the taxes.

Using money from the IRA itself to pay the tax reduces the amount that can continue growing tax-deferred, diminishing the potential benefits of the conversion.

We prefer to keep our assets invested and growing rather than liquidating a portion to cover taxes now. This approach aligns with our long-term financial goals and risk tolerance.

How Roth IRA Conversions Get Taxed

When you convert a Traditional IRA to a Roth IRA, the entire converted amount is subject to taxes as ordinary income, not just any gains made on the account.

This means that the full balance, both the original contributions (if they were pre-tax) and the earnings, will be taxed at your ordinary income tax rate.

It’s important to note that this rate is not the more favorable capital gains rate, which applies to long-term investments, but instead is the same rate you pay on your regular salary, bonuses, or business income.

For example, if you convert $100,000 from a Traditional IRA to a Roth IRA, and your tax bracket is 24%, you will owe $24,000 in taxes on that conversion, regardless of how much of that $100,000 is from gains or contributions.

This is a crucial point to understand because many people mistakenly believe that only the gains in the account will be taxed.

Roth conversions treat the entire conversion amount as ordinary income, potentially increasing your taxable income significantly in the year of conversion and even pushing you into a higher tax bracket.

Before deciding to convert, consider how much income this conversion will add to your total for the year and plan accordingly to avoid unintended tax consequences.

The Time Value of Money: Comparing Roth and Traditional IRAs Through Calculations

An important aspect of choosing between a Roth IRA and a Traditional IRA is understanding how the time value of money and taxes affect your retirement savings. Interestingly, when tax brackets remain the same now and in retirement, the end result of both accounts can be identical.

But is this really accurate? Let’s delve into some calculations to illustrate this point and explore scenarios where tax brackets change over time.

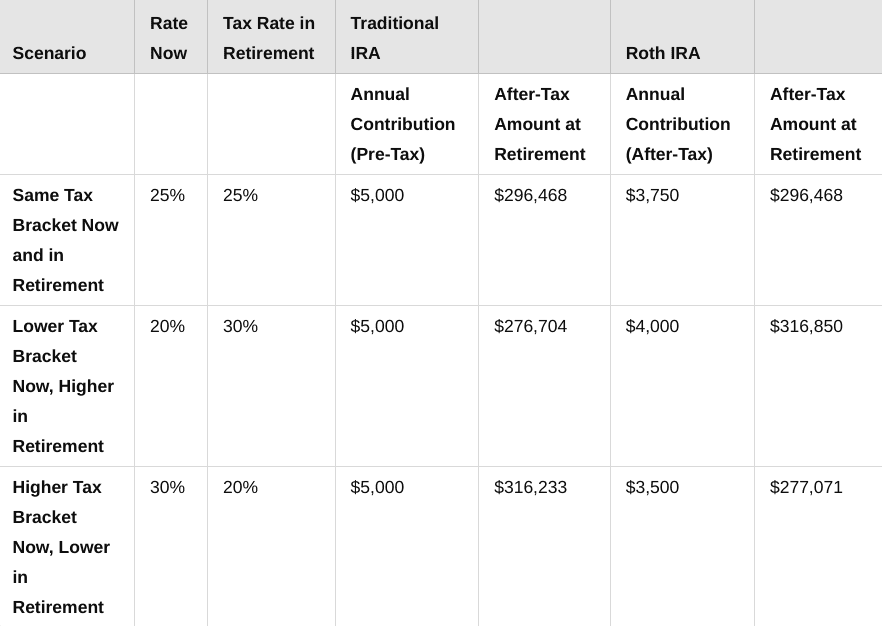

Same Tax Bracket Now and in Retirement

Let’s consider a simplified example where the tax rate is the same during your working years and in retirement.

Suppose you have $5,000 to invest annually for retirement, and your tax rate is 25% both now and in retirement. Let’s assume an annual investment return of 6% over 30 years.

Traditional IRA:

You contribute the full $5,000 pre-tax each year. Over 30 years at 6%, your account grows to:

- Future Value:

$5,000 × \((1 + 0.06)^{30} – 1\) ÷ 0.06 ≈ $395,291

Upon retirement, you withdraw the funds and pay 25% tax:

- After-Tax Amount:

$395,291 × (1 – 0.25) = $296,468

Roth IRA:

You pay taxes upfront, so your net contribution is:

- Net Contribution:

$5,000 × (1 – 0.25) = $3,750

Over 30 years at 6%, your account grows to:

- Future Value:

$3,750 × \((1 + 0.06)^{30} – 1\) ÷ 0.06 ≈ $296,468

Withdrawals are tax-free, so you have $296,468.

Result: In both cases, you end up with $296,468 after taxes, demonstrating that when tax rates are the same now and in retirement, the Traditional and Roth IRAs can yield the same after-tax amount.

Lower Tax Bracket Now, Higher in Retirement

Now, let’s consider a scenario where you are in a lower tax bracket now (20%) and expect to be in a higher tax bracket in retirement (30%).

Traditional IRA:

You contribute the full $5,000 pre-tax each year. Your account grows to approximately $395,291 over 30 years.

Upon retirement, you pay 30% tax on withdrawals:

- After-Tax Amount:

$395,291 × (1 – 0.30) = $276,704

Roth IRA:

Your net contribution after paying 20% tax is:

- Net Contribution:

$5,000 × (1 – 0.20) = $4,000

Your account grows to:

- Future Value:

$4,000 × \((1 + 0.06)^{30} – 1\) ÷ 0.06 ≈ $316,850

Withdrawals are tax-free, so you have $316,850.

Result: The Roth IRA provides a higher after-tax amount because you paid taxes at a lower rate upfront and avoided paying taxes at a higher rate in retirement.

Higher Tax Bracket Now, Lower in Retirement

Finally, let’s examine the scenario where you are in a higher tax bracket now (30%) and expect to be in a lower tax bracket in retirement (20%).

Traditional IRA:

You contribute the full $5,000 pre-tax each year. Your account grows to approximately $395,291 over 30 years.

Upon retirement, you pay 20% tax on withdrawals:

- After-Tax Amount:

$395,291 × (1 – 0.20) = $316,233

Roth IRA:

Your net contribution after paying 30% tax is:

- Net Contribution:

$5,000 × (1 – 0.30) = $3,500

Your account grows to:

- Future Value:

$3,500 × \((1 + 0.06)^{30} – 1\) ÷ 0.06 ≈ $277,071

Withdrawals are tax-free, so you have $277,071.

Result: The Traditional IRA yields a higher after-tax amount because you deferred taxes at a higher rate and paid them at a lower rate in retirement. With the Roth IRA, you paid taxes upfront at a higher rate.

Table Comparing Roth and Traditional IRAs In Different Tax Environments

These calculations illustrate that when tax rates remain the same, the Roth and Traditional IRAs can produce identical after-tax results due to the time value of money.

When tax rates differ between your working years and retirement, the timing of taxation becomes crucial. Paying taxes when rates are lower, either now or later, can significantly impact your retirement savings.

This reinforces the importance of considering your current and expected future tax situations when choosing between a Roth and a Traditional IRA.

The Importance of Personalized Financial Advice

My campfire debate with my cousin highlighted a critical issue in financial planning: the necessity of personalized advice. Financial strategies should never be one-size-fits-all.

Advisors must conduct thorough discovery to understand a client’s income, assets, liabilities, goals, and risk tolerance before making recommendations.

Generalized advice can lead to suboptimal or even detrimental financial decisions. In my experience, both personally and professionally, tailored strategies yield the best outcomes.

It’s essential to work with advisors who take the time to understand your unique situation rather than pushing generic solutions.

Should Everyone Do A Roth IRA Conversion? No.

Roth IRAs offer valuable benefits, but they’re not universally superior to Traditional IRAs. The decision to contribute to or convert into a Roth IRA should be based on a comprehensive analysis of your current financial situation and future expectations.

For individuals like me, with significant assets in taxable accounts and an anticipated lower tax bracket in retirement, sticking with a Traditional IRA may be more advantageous. It allows for tax-deferred growth now and potentially lower taxes on withdrawals later.

It provides opportunities to manage RMDs strategically, aligning with our broader financial and philanthropic goals.

Before making any decisions about retirement accounts, consult with a qualified financial advisor who prioritizes understanding your personal circumstances. Avoid the trap of generic advice that doesn’t account for your unique needs.

So, the next time you’re around a campfire—or scrolling through social media—and someone insists that a Roth IRA is the best choice for you, remember that personal finance is just that: personal. Make informed decisions based on thorough research and professional guidance tailored to your situation.

🙋♂️Ready to take charge of your financial future? Subscribe to the DadisFIRE newsletter and follow Dad is FIRE on YouTube for more insights on financial independence and smart money management.💪