How Likely Is The IRS To Audit You? An Experienced CPA Answers

Taxes are a headache. Audits are worse. Nobody wants to deal with the IRS sending a letter, asking for records, and possibly demanding more money. But is an audit something most people should actually worry about?

My CPA friend Bo from The Crunch has gone through IRS audit data to separate fact from fiction. Bo knows his stuff. If you want smarter tax insights, follow him on X at The Money Cruncher, CPA.

Today, we’re breaking down the real odds of getting audited based on Bo’s deep dive into actual statistics, income levels, and IRS priorities. We’ll look at which income brackets are most at risk, why certain returns get flagged, and what happens if the IRS comes knocking.

If you’ve ever wondered how much the IRS actually cares about your tax return, this is the breakdown you need.

Table of Contents

What Are the Odds of an IRS Audit?

Most people assume the IRS is lurking in the shadows, waiting to pounce on their tax return. In reality, based on Bo’s research, only 0.44% of tax returns were audited between 2013 and 2021. That’s about 1 in 227, which means the vast majority of taxpayers fly under the radar.

While audits do happen, they’re not nearly as common as some would like you to believe. But not all tax returns are treated the same. Some people are way more likely to get audited than others, and income plays a massive role.

The IRS isn’t randomly picking names out of a hat. They focus on certain groups more than others, and understanding where you fall in that mix is key.

Maximize Your Refund: 18 Often-Overlooked Tax Deductions Worth Checking Before Filing

IRS Audit Rates Based on Income Level

The idea that “rich people never get audited” isn’t exactly true, but neither is the belief that “the IRS only goes after the little guy.” The real story is a bit more nuanced. Based on Bo’s findings, the audit rate isn’t linear.

The lowest and highest income brackets see more audits, while the middle gets a pass. For 2021, taxpayers with no positive income faced a 0.3% audit rate. Those making $1 to $25,000 had a 0.4% audit rate.

Meanwhile, if someone made $25,000 to $50,000, their odds dropped to 0.2%, and audit risk continued falling until hitting the $500,000 range. This means someone earning under $25,000 was actually four times more likely to be audited than someone making $200,000 to $500,000.

On the other end, ultra-high-income earners start seeing audit rates shoot up. The IRS paid special attention to those making $5M+, with 8.7% of $10M+ earners audited between 2013-2021. The numbers don’t lie, the more complex the return, the more scrutiny it gets.

🙋♂️If this is interesting so far, follow DadisFIRE on Medium, then hit like to see more articles on financial freedom, personal finance, and smart money moves.💪

Why Low-Income Earners Get Audited More Often

Most people assume the IRS is chasing billionaires. In reality, those earning under $25,000 are targeted more often than some six-figure earners. This isn’t about punishing the poor, it’s about fraud detection.

The Earned Income Tax Credit (EITC) is one of the most misused tax benefits, and the IRS knows it. The CPA highlighted that tax returns claiming the EITC had a 0.7% audit rate, one of the highest among all tax brackets.

The IRS aggressively checks these filings because fraudulent claims are common. That doesn’t mean every low-income filer is lying, but the IRS has seen enough false EITC claims to make it a high-risk category. If an audit letter shows up, this tax credit is often the reason.

Give Yourself A Gift Instead of Uncle Sam: 18 Smart Tax Tips

Why Ultra-High-Income Earners Get Audited More

Making millions doesn’t automatically trigger an audit, but once income crosses the $5M mark, the IRS starts paying close attention. The wealthiest filers are more likely to have complicated tax returns with deductions, offshore accounts, trusts, and business write-offs that the IRS wants to double-check.

Based on Bo’s analysis, 8.7% of $10M+ earners faced audits over a nine-year span. That’s a big jump compared to most income brackets.

The IRS isn’t necessarily out to punish success, but they know that tax loopholes, aggressive deductions, and potential underreporting are far more common at this level.

Don’t Let the IRS Take More Than They Should: 15 Smart Tax Moves W2 Workers Can Use

How IRS Audit Rates Have Shifted Over Time

Audits aren’t set in stone. They fluctuate based on IRS staffing, funding, and political priorities. The CPA looked at data showing that audit rates steadily declined between 2014 and 2020 due to budget cuts and fewer IRS agents.

Things picked up a bit in 2021 and 2022, but then audit activity dropped off again in 2023. This means past audit trends don’t guarantee future patterns. If IRS funding increases, audits could ramp up again. If Congress cuts IRS resources, audits might keep shrinking.

The numbers aren’t set in stone, but the general trend has been fewer audits in recent years compared to the past.

What Happens If You Get Audited?

Most audits don’t involve an IRS agent showing up at the door. In fact, 77.3% of audits are handled through correspondence, meaning the IRS sends a letter, asks for proof, and then issues a final ruling. It’s rarely dramatic.

For most taxpayers, an audit is just an annoying paperwork process. Higher-income taxpayers, especially those making $5M+, are more likely to face field audits, actual face-to-face meetings with IRS agents.

These tend to be more intense and time-consuming, but unless fraud is involved, most audits just result in adjustments and additional taxes owed.

Avoid Tax Trouble: 18 Common Audit Triggers That Could Land You on the IRS Watchlist

Do Most IRS Audits Lead to More Taxes Owed?

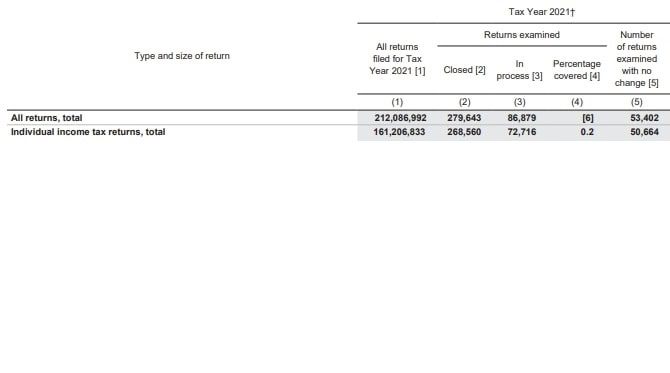

Getting audited doesn’t always mean owing money, but 80% of audited taxpayers ended up paying something extra. Out of 268,560 closed audits in 2021, around 50,664 resulted in no changes, meaning 20% walked away without owing a dime.

That said, most people do end up paying more after an audit. The IRS typically finds something to adjust, be it a deduction that gets denied, missing income, or an error that needs correcting.

It’s not always a massive bill, but the IRS rarely audits someone just to tell them, “You did everything perfectly!”

🙋♂️If you like what you are reading so far, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube.💪

Does an Audit Mean the IRS Will Come to Your House?

The idea of IRS agents banging on the door makes for good TV, but it’s not how audits work for most people. Based on Bo’s research, the IRS conducts over 75% of audits remotely. The agency sends a letter, the taxpayer responds, and that’s the end of it.

The only taxpayers facing in-person field audits tend to be high-net-worth individuals, specifically those making $5M+. If someone is pulling in that level of income, they might get an IRS visit.

But for the average taxpayer, an audit means dealing with paperwork, not an agent knocking at the door.

The Tax Perks of Aging: 19 Tax Breaks You Can Claim After 50

How to Lower the Chances of an Audit

The IRS isn’t hunting for innocent taxpayers, it’s looking for red flags. Common triggers include math errors, unusually high deductions, unreported income, and suspicious business write-offs.

Keeping accurate records, using tax software, and working with a CPA can help avoid mistakes that might get flagged.

Save on Taxes: 19 Smart Ways to Keep More of Your Money

Should You Worry About an Audit?

For most people, the audit risk is incredibly low. If you’re making between $25,000 and $500,000, odds are slim to none. The IRS focuses on low-income returns claiming credits and ultra-wealthy filers with complex returns.

As long as taxes are filed accurately and honestly, the chances of getting audited and owing more money remain minimal.

The Reality of IRS Audits

Most people stress about audits way more than they need to. The odds are low unless income falls into a high-risk category, like claiming certain tax credits or pulling in millions. Even when audits happen, most are handled through the mail and don’t lead to massive tax bills.

The best way to stay in the clear is to file an honest return, keep solid records, and avoid sketchy deductions. The IRS isn’t randomly targeting everyday taxpayers, it’s looking for patterns, red flags, and errors that stand out.

If everything checks out, there’s nothing to worry about.

Big thanks to Bo at The Crunch for breaking it all down. For more smart tax insights, follow him on X at The Money Cruncher, CPA.

🙋♂️If you like what you just read, subscribe to the DadisFIRE newsletter and follow DadisFIRE on YouTube. 💪 Also be sure to follow DadisFIRE on Medium💰